Rithmic API is a powerful tool for futures prop traders, offering ultra-fast tick-by-tick market data and lightning-speed order execution. It connects directly to major exchanges like CME and ICE, delivering unfiltered data with microsecond precision. This makes it a go-to for traders using scalping strategies at top prop firms or managing multiple accounts with trade copiers. Key features include:

- Tick-by-tick data: Every price change is captured without aggregation.

- Market By Order (MBO) data: View individual orders instead of grouped price levels.

- Server-side order management: Bracket orders, trailing stops, and OCO orders stay active even during local issues.

- API options: From R | API+ for custom trading solutions to R | Diamond API for ultra-low latency, Rithmic supports a range of trading needs.

Rithmic is widely integrated with platforms like NinjaTrader, Sierra Chart, and Bookmap, and supports futures prop firms such as Apex Trader Funding and Topstep. Whether you’re automating trades, managing multi-account setups, or scalping, Rithmic’s infrastructure ensures speed and reliability.

| API Type | Best Use Case | Latency | Monthly Cost |

|---|---|---|---|

| **R | API+** | Automated systems with risk tools | ~250µs |

| **R | Diamond** | High-frequency trading & scalping | <250µs |

| **R | FIX API** | Institutional order routing | ~250µs |

| **R | Trader Pro** | Prototyping & lightweight automation | Standard |

Rithmic’s tools are essential for traders who demand precision, speed, and reliability in futures trading.

Core Features of Rithmic API for Futures Prop Traders

Real-Time and Historical Market Data

Rithmic provides unfiltered tick data, capturing every bid, ask, and trade without the typical smoothing or filtering found in retail feeds. Each market event is timestamped with microsecond precision – and in some configurations, nanosecond accuracy. This level of detail is invaluable for measuring order transmission speeds and pinpointing execution slippage, which is especially important for automated systems managing multiple prop trading accounts. Additionally, the platform offers historical tick-level data, allowing traders to thoroughly backtest automated strategies. This robust data infrastructure supports precise order execution and effective risk management.

Order Execution and Risk Management

Rithmic handles bracket orders, OCO (one-cancels-other), and trailing stops directly on its servers. This server-side functionality ensures that protective stops remain active even if your computer or internet connection fails – crucial for automation systems adhering to daily loss limits at firms like Apex Trader Funding and Topstep. With tick-to-trade execution speeds under 250 microseconds, the API delivers institutional-grade performance, minimizing the risk of severe account losses during technical disruptions. This reliable execution framework also enhances the platform’s ability to provide advanced market insights for strategic automation.

Advanced Market Insights

Rithmic’s Market by Order (MBO) data offers a detailed view of individual orders instead of aggregated price levels, making it easier for automated systems to distinguish between institutional activity and smaller retail orders. This granular order flow data helps automation software make smarter entry and exit decisions based on real market depth. Additionally, Rithmic’s two-way Excel integration through R | Trader Pro allows live data streaming into spreadsheets for creating custom indicators and executing trades directly. This feature streamlines the prototyping of automated strategies before full API deployment. The platform’s infrastructure can process over 100,000 messages per second during high-volatility periods, all while maintaining nanosecond-precision timestamps. This ensures that automation systems can efficiently handle high-frequency trade copying across multiple prop accounts without delays or data bottlenecks.

sbb-itb-46ae61d

UNLOCK Pro Futures Trading: The Rhythmic API, Python & AI Path to HFT

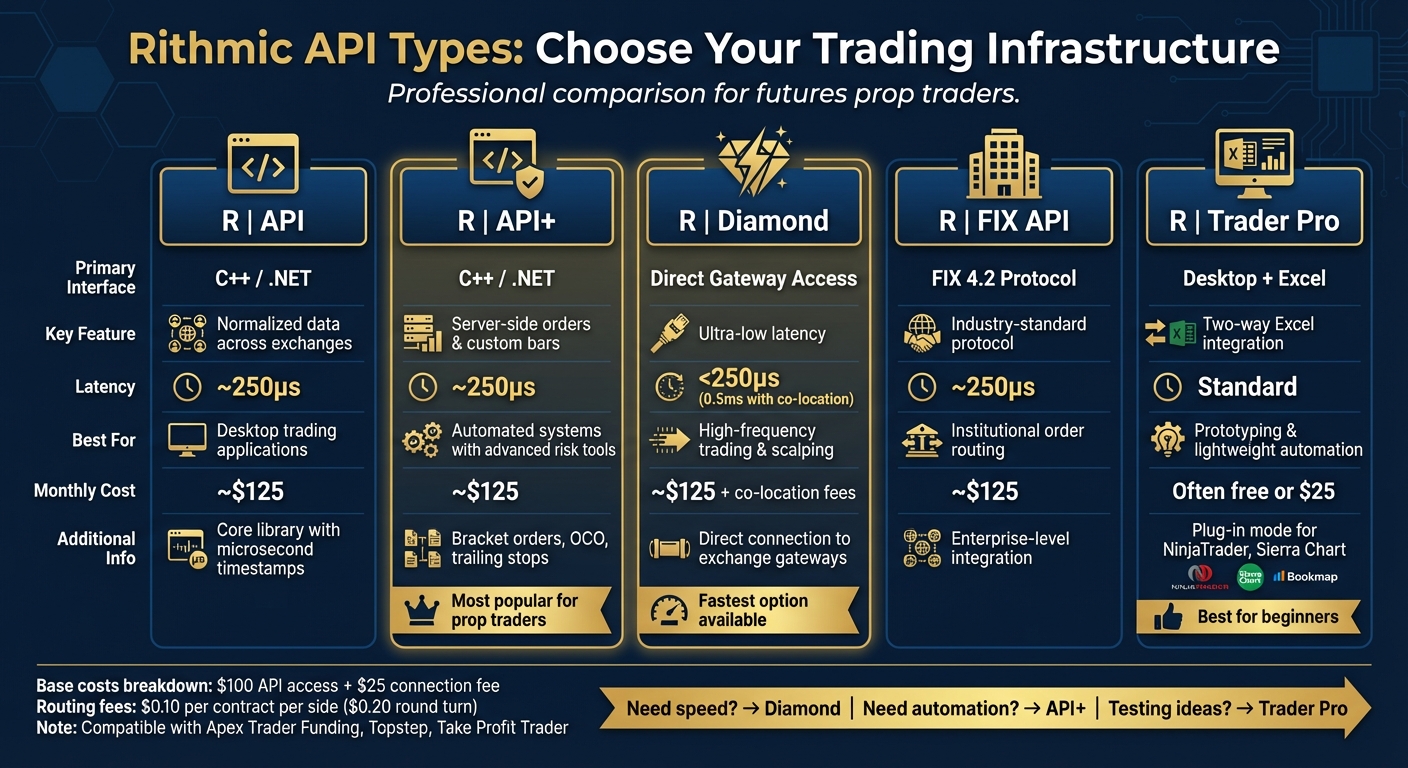

Rithmic API Types and Their Use Cases

Rithmic API Types Comparison: Features, Latency, and Pricing Guide

Rithmic offers API options tailored for futures prop traders, addressing different needs for automation and speed. Choosing the right API can save both time and money during development.

R | API and R | API+

R | API serves as the core library, compatible with C++ and .NET. It provides normalized market data and order reports with microsecond timestamps from all supported exchanges. This design eliminates the hassle of handling exchange-specific logic, simplifying trading across multiple markets.

R | API+ builds on this foundation by adding server-side order management and custom bar generation. Features like bracket orders, OCO (one-cancels-other), and trailing stops are managed on Rithmic’s servers, ensuring stability even during connectivity issues. This is particularly useful for traders working with firms like Apex Trader Funding or Take Profit Trader, where maintaining daily loss limits is critical. Additionally, R | API+ can produce tick, volume, and range bars directly on the server, reducing the load on your local system.

The pricing includes $100 per User ID for API access (supporting up to five simultaneous platform connections) and a $25 base connection fee. Routing costs are approximately $0.10 per contract per side (or $0.20 round turn).

For traders who need even faster performance, the R | Diamond API is the next step.

R | Diamond API for Ultra-Low Latency

R | Diamond API is designed for high-frequency trading and scalping, where every microsecond counts. Unlike standard APIs that rely on Rithmic’s ticker plant, Diamond connects directly to market data handlers and exchange-facing gateways. This architecture achieves transit times – from market data processing to order release – of under 250 microseconds.

"Traders using Diamond Programs™ realize transit times… of less than 250 microseconds." – AMP Futures

One standout feature is the "held order" mechanism. Orders are pre-staged at Rithmic’s exchange-facing gateways after passing risk checks, and only a minimal "release" signal is sent when triggered. This is ideal for strategies where order queue position is critical. Co-locating servers at the Aurora data center near the CME can further reduce latency to 0.5ms, compared to the 14–18ms typical of remote connections.

Diamond’s pricing mirrors R | API+ costs, but full utilization requires investing in co-location and infrastructure.

R | FIX API and Desktop Integration

R | FIX API operates on the FIX 4.2 protocol, making it suitable for institutional systems or developers working with standardized financial protocols. While less common for retail automation, it’s a solid choice for integrating with enterprise-level trading setups.

For desktop users on platforms like NinjaTrader, Tickblaze, or Quantower, R | Trader Pro acts as a bridge. When run in "Plug-in Mode", it connects third-party platforms to Rithmic’s data and execution services. Additionally, its two-way Excel integration allows users to build indicators, perform calculations, and automate trades directly within spreadsheets.

"Two-way communication with Microsoft Excel means you can build indicators, run calculations, and even automate trades using Excel formulas. For quants who live in spreadsheets, this is powerful." – PropFirmApp

R | Trader Pro is often free with a Rithmic data subscription, though some brokers charge $25 per month for advanced features like chart-based trading. When setting up, ensure "Allow Plugins" is enabled in the R | Trader Pro login screen, and that plug-in settings match on both platforms to avoid connection issues.

| API Type | Primary Interface | Key Advantage | Best Use Case | Monthly Cost |

|---|---|---|---|---|

| R | API | C++ / .NET | Normalized data across exchanges | Desktop trading applications | ~$125 |

| R | API+ | C++ / .NET | Server-side orders & custom bars | Automated systems with advanced risk tools | ~$125 |

| R | Diamond | Direct Gateway Access | Ultra-low latency (<250µs) | High-frequency trading & scalping | ~$125 + co-location |

| R | FIX API | FIX 4.2 Protocol | Industry-standard protocol | Institutional order routing | ~$125 |

| R | Trader Pro | Desktop + Excel | Two-way Excel integration | Prototyping & lightweight automation | Often free or $25 |

Base costs include $100 API access + $25 connection fee; routing fees are $0.10 per contract per side.

Building Automation and Multi-Account Solutions with Rithmic

How to Structure an Automated Futures Trading System

Setting up an automated futures trading system with Rithmic starts with choosing the right API for your needs. Options include R | API+ for general programmatic access, R | Protocol API for WebSocket-based web or mobile integrations, and R | Diamond API for ultra-low latency requirements. To achieve the best performance, it’s recommended to place your automated programs in data centers like TheOmne.net, reducing exchange latency. For those using R | Diamond API, this setup can deliver transit times under 250 microseconds for executing automation strategies.

A typical cloud-based workflow might involve a TradingView alert triggering a webhook. This webhook sends a JSON payload to a bridge (such as PickMyTrade), which then executes the order using the Rithmic API. One critical detail: ensure you use the exact system name provided by your proprietary trading firm (e.g., "Rithmic 01"). Using incorrect identifiers can lead to connection issues. Also, make sure your Windows clock is synced via the "Sync now" feature in the Time & Language settings to avoid logon errors.

Trade Copying and Multi-Account Management

Once your system is up and running, trade copying tools become a key feature for managing multiple accounts. Tools like SyncFutures or Copilink allow you to execute a trade on a "master" account and replicate it across multiple "slave" accounts in milliseconds. This is especially helpful when trading across accounts from firms like Apex Trader Funding or Take Profit Trader. Rithmic’s credential-based authentication ensures seamless synchronization.

To manage accounts of different sizes, configure quantity multipliers. For example, placing 1 contract on a $50,000 account could automatically replicate as 2 contracts on a $100,000 account. Before scaling up, it’s wise to test the replication process with a micro contract to confirm that trades execute simultaneously. Keep in mind that Rithmic retail-tier accounts have a weekly data cap of about 40 GB. If you’re running high-bandwidth strategies, like those using DOM or footprint charts across multiple accounts, you may encounter slower updates due to throttling.

With trade copying in place, the next step is to focus on risk management to ensure long-term success.

Risk and Compliance for Prop Trading Automation

Rithmic’s server-side order management tools make it easier to enforce strict risk protocols. Features like trailing stops, brackets, and OCO (one-cancels-other) orders are managed directly on the server. This is particularly important for staying compliant with the rules set by proprietary trading firms. For example, firms like Apex Trader Funding, which has paid out over $550 million in trader compensation since 2022, require traders to adhere to strict daily loss limits.

"Subject to pre‐trade risk management parameters (set by the FCM), evaluated by the exchange facing gateway, the order is sent to the exchange." – Rithmic

The R | Trader Pro dashboard offers real-time tracking of trailing drawdowns and daily P&L. For automated systems, it’s essential to include cooldown filters to prevent duplicate orders. Additionally, always set Stop-Loss (SL) and Take-Profit (TP) parameters in automated alerts to ensure compliance with prop firm risk rules. When integrating R | Trader Pro with platforms like NinjaTrader, enable "Allow Plugins" in Rithmic and "Plug-in Mode" in the trading platform to maintain smooth data flow.

Choosing Futures Prop Firms That Use Rithmic

Why Rithmic Matters for Futures Prop Firms

Rithmic serves as the backbone for many top-tier futures prop firms, offering real-time enforcement of drawdown and position limits. This server-side automation ensures that stops and targets remain active, even if there are local connection issues. For firms managing large groups of traders, this level of automated protection is essential to safeguard both firm capital and individual accounts.

With tick-to-trade speeds clocking in at under 250 microseconds, Rithmic provides a significant edge for scalpers and algorithmic traders during periods of high market volatility. Additionally, firms using Rithmic often include advanced tools like R | BASS and full Depth of Market functionality through R | Trader Pro.

These features make Rithmic a critical factor when evaluating futures prop firms.

Top Futures Prop Firms Recommended by DamnPropFirms

Apex Trader Funding: Apex supports up to 20 accounts and has paid out over $600 million to traders. It provides direct Rithmic credentials compatible with popular platforms like NinjaTrader, Bookmap, and Sierra Chart, ensuring smooth execution. The firm uses an unrealized trailing drawdown model and frequently offers discounts of 80–90% on evaluation fees. DamnPropFirms members can access up to 90% off using code DGT.

Take Profit Trader: Known for its fair rules and realistic trading conditions, this firm employs an End-of-Day (EOD) drawdown model during evaluations and eliminates consistency rules once traders are funded. It offers no activation fees, daily withdrawals, and the ability to copy trades across up to 5 live funded accounts. Members can save 40% using code DGT.

FundedNext Futures: FundedNext offers fast payouts (3–5 days) and allows up to 12 accounts without imposing consistency rules at the funded stage. Its Bolt plan permits withdrawals starting on Day 1, while Rapid accounts can qualify in a single day.

Alpha Futures: Alpha Futures stands out with payout caps of $15,000 per week per account on its Advanced plans, though traders are limited to 3 accounts.

Instant Funding and Automation Options

If you’re looking for immediate trading capital, these options deliver instant funding with Rithmic integration.

Lucid Trading: LucidDirect accounts offer a 90/10 profit split with no evaluation or activation fees, though they enforce a 20% consistency rule. Members can save up to 50% using code DGT.

Tradeify: Tradeify’s Lightning instant funding plan allows traders to choose their account type. It uses an EOD drawdown model and applies a 20–30% consistency rule during scaling, with a cap of 5 accounts per trader. Paired with trade copiers like Tradesyncer, traders can synchronize one master account with over 40 follower accounts across multiple firms. Members save 30% with code DGT.

"Rithmic is widely regarded as one of the fastest and most stable data feeds available for futures traders, especially for scalping, DOM-based trading, and algorithmic strategies." – Fred Harrington, Founder of Vetted Prop Firms

Conclusion and Practical Checklist for Rithmic Integration

Key Takeaways

Rithmic handles 20% of the global daily futures volume, delivering tick-to-trade execution in under 250 microseconds. Its server-side order management and unfiltered tick-by-tick data provide the backbone for professional futures prop trading, ensuring resilience against local connection issues. These features make it an essential tool for building reliable, automated trading systems.

Selecting the right API is crucial for achieving the desired performance. Whether you’re using R | API+ for Python to develop automated systems or R | Diamond API for ultra-low latency scalping, the choice has a direct impact on execution quality. Many top-rated firms listed on DamnPropFirms offer direct Rithmic credentials, enabling smooth integration with platforms like NinjaTrader, Sierra Chart, and Bookmap.

Here’s a practical checklist to help you integrate Rithmic effectively.

Checklist for Rithmic Setup

- Before Connecting:

- Log into R | Trader Pro to complete required exchange agreements and select "Non-Professional" status to avoid high data fees.

- Synchronize your Windows clock (Settings > Time & Language > Sync Now) to prevent authentication issues.

- During Platform Configuration:

- Enable "Allow Plugins" in R | Trader Pro and connect your trading platform using Plug-in Mode.

- Verify that the "System Name" matches your prop firm’s server identifier to avoid connection errors.

- Enable "Sync Positions with Broker" in your trading software to ensure PnL and position data are aligned, reducing the risk of ghost trades.

- For Multi-Account Management:

- Test with a single micro contract to confirm replication speed and consistency.

- If managing accounts with firms like Apex Trader Funding (up to 20 accounts) or Take Profit Trader (up to 5 accounts), use the

list_accounts()method to retrieve active account IDs. This step ensures smooth integration with trade copying and risk management strategies.

"Think of Rithmic as the engine that powers your car; you don’t drive the engine directly, but without it, you’re not going anywhere." – PropFirmApp

- Maintenance:

- Restart your trading platform daily, preferably during lunch or after market hours, to clear memory bloat and refresh data connections.

- Use a wired Ethernet connection instead of Wi-Fi to reduce latency jitter by 5–15ms.

FAQs

Which Rithmic API should I use for my strategy?

For real-time data and automation, the async_rithmic Market Data API is a great choice for accessing market data, performing symbol searches, and checking exchange listings. On the other hand, the R | API+™ offers normalized market data, order management capabilities, and execution reports, making it suitable for more extensive platform integration. The right option depends on whether your focus is on real-time data access or a more complete order management solution.

Do server-side bracket and OCO orders still work if I disconnect?

Yes, server-side bracket and OCO orders will continue to function even if you lose connection. However, it’s important to note that Rithmic’s OCO orders are locally simulated and depend on an active connection. If you get disconnected, the remaining orders in an OCO group won’t be canceled automatically after one of them is executed.

What setup changes actually reduce latency with Rithmic?

To minimize latency when using Rithmic, start by installing R|Trader Pro and enabling plugin bridging. Then, focus on optimizing your connections to platforms such as NinjaTrader or Quantower. For detailed instructions, refer to the setup guide provided on DamnPropFirms. Following these steps will help ensure a faster and more seamless trading experience.