Dynamic sizing is a trading strategy that helps you manage risk and grow funded accounts by adjusting position sizes based on market conditions, account performance, and trade quality. It’s especially useful for meeting the strict rules of proprietary trading firms, such as drawdown limits and consistency requirements. Here’s the essence of how it works:

- Risk Consistency: Always risk a fixed percentage of your account, like 1-2%, ensuring your position size scales with account growth or shrinkage.

- Volatility Adjustments: Use tools like the Average True Range (ATR) to reduce position size when market volatility increases, protecting your account from unnecessary losses.

- Trade Quality Assessment: Adjust risk based on the strength of your trade setup. For example, risk more on high-probability trades and less on weaker ones.

- Portfolio Management: Limit overall exposure by managing multiple strategies and accounts, ensuring total risk stays within 4-8% of your account balance.

Dynamic Position Sizing in Futures Trading

sbb-itb-46ae61d

Core Principles of Dynamic Sizing

Dynamic sizing revolves around three key ideas: keeping risk as a consistent percentage, adjusting for changes in market volatility, and assessing trade quality. Together, these principles help protect your account while enabling steady growth through disciplined risk management.

Maintaining Consistent Percentage Risk

At its core, dynamic sizing is about risking the same percentage of your account on every trade – usually 1-2%. This method ensures your position size adjusts as your account grows. For example, if you start with a $100,000 account and risk 1%, you’re risking $1,000 per trade. When your account increases to $110,000, that same 1% becomes $1,100, automatically scaling your position size while maintaining the same level of risk [8].

The formula for calculating position size is straightforward:

(Account Capital × % Risk) ÷ (Stop Loss Distance × Value per Point) [1][8].

For instance, trading ES futures with one of the best futures prop firms using a trading ES futures with a $100,000 account00,000 account, risking 1% ($1,000), and setting a stop 10 points away, results in 2 contracts:

1,000 ÷ (10 × 50) = 2.

"You can have the world’s best strategy. If you size wrong, you die." – Van Tharp, Trading Legend [8]

This approach naturally adapts as market conditions fluctuate.

Adjusting for Market Volatility

Volatility often signals shifts in market behavior. When the Average True Range (ATR) expands, stop-loss levels must increase to avoid unnecessary exits. To maintain the same dollar risk, position sizes need to shrink as volatility rises [1][6].

A practical adjustment method involves monitoring ATR. For example:

- If the 14-day ATR exceeds its 6-month median, reduce trade risk by 25-50% [1].

- If ATR jumps by 50%, consider cutting position size by 30-40% [3].

This inverse relationship between volatility and position size helps stabilize risk during turbulent periods. For equity traders, similar adjustments can be made using VIX levels to manage exposure effectively [1].

Evaluating Trade Quality

Beyond consistent risk and volatility adjustments, trade sizing should reflect the strength of your setup. Historical performance and current conditions play a critical role in determining how much to risk [4].

For instance, if your trend-following strategy has a 55% win rate in trending markets but drops to 40% in choppy conditions, you might risk a full 1% in favorable conditions but scale down to 0.5% or even skip trades in less favorable ones. This ensures your risk aligns with the setup’s probability [1][4].

The risk-to-reward ratio is equally important. A strategy with a 45% win rate but a 3:1 reward-to-risk ratio can still succeed – provided you size conservatively enough to withstand losing streaks [4][6]. For strategies with lower win rates and reward-to-risk metrics, reducing position size even further is essential to safeguard your account.

Recent trade performance also serves as a guide. After consecutive losses, your accuracy may dip due to changing market conditions. In such cases, reducing position size is wise until you recover 50-100% of the losses [2][3]. Only then should you consider scaling back up.

Even when a trade setup looks perfect, rely on its historical performance rather than instinct [4][5]. Sticking to disciplined position sizing is what sustains long-term success.

How to Implement Dynamic Sizing

Dynamic Position Sizing Formula and Risk Management Framework for Funded Trading Accounts

Dynamic sizing is all about adjusting your position sizes based on risk and volatility, ensuring consistent exposure across trades. Here’s how you can put this into action by calculating position sizes, applying it across strategies, and managing your overall portfolio risk.

Calculating Position Size for Each Trade

The starting point for dynamic sizing is this formula:

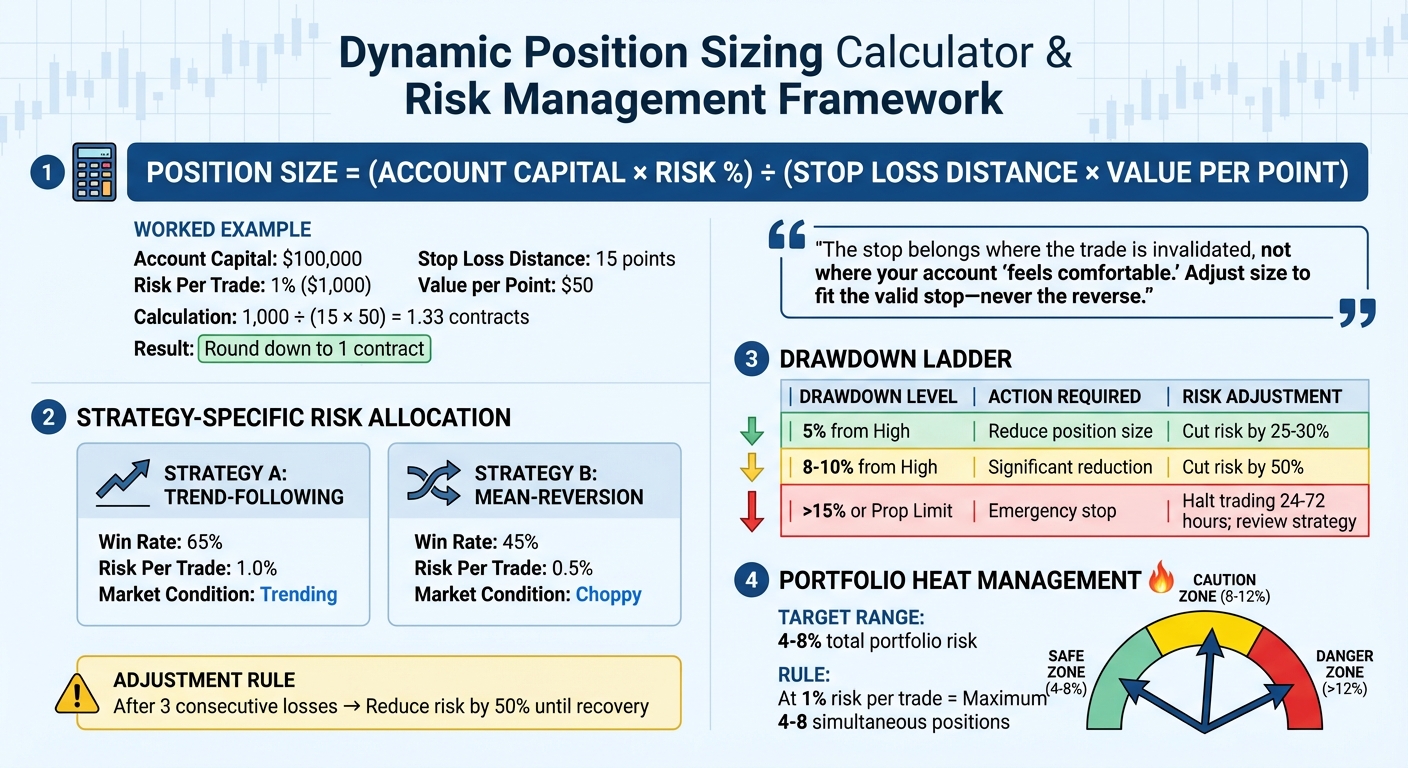

Position Size = (Account Capital × Risk %) ÷ (Stop Loss Distance × Value per Point) [8]

This method keeps your dollar risk consistent, no matter where your stop-loss is placed. Let’s break it down with an example:

Imagine you’re trading ES futures with a $100,000 account, risking 1% per trade (or $1,000). If your setup requires a 15-point stop and ES moves $50 per point, here’s the calculation:

1,000 ÷ (15 × 50) = 1.33 contracts

Since fractional contracts aren’t a thing, you’d round down to 1 contract. Always calculate your risk in dollars first to ensure your maximum loss per trade is fixed.

"The stop belongs where the trade is invalidated, not where your account ‘feels comfortable.’ Adjust size to fit the valid stop – never the reverse." – International Trading Institute [1]

Once you’ve calibrated risk for individual trades, you can extend these principles to multiple strategies.

Applying Dynamic Sizing Across Multiple Strategies

Dynamic sizing isn’t limited to a single trade. When juggling multiple strategies, each should have its own risk allocation based on its performance and market conditions. For example:

- A trend-following strategy with a 65% win rate might justify risking 1% per trade.

- Meanwhile, a mean-reversion strategy with a 45% win rate might only warrant 0.5% risk.

Adjust these allocations in real time. If a strategy experiences three consecutive losses, reduce its risk by 50% until it recovers. Also, factor in correlations between assets – closely related positions should be evaluated together to prevent overexposure.

With individual risks adjusted, the next step is managing your total portfolio exposure.

Managing Portfolio-Level Risk

Portfolio heat, or the total percentage of your account at risk across all open positions, should stay between 4% and 8%. For instance, if you’re risking 1% per trade, limit yourself to 4–8 simultaneous positions to avoid excessive risk.

To handle losing streaks, use a drawdown ladder to adjust risk systematically:

| Drawdown Level | Action Required |

|---|---|

| 5% from High | Reduce risk per trade by 25–30% |

| 8–10% from High | Reduce risk per trade by 50% |

| >15% or Prop Limit | Halt trading for 24–72 hours; review your strategy |

This approach takes emotion out of the equation. For example, if your equity drops by 5%, cut position sizes by 25–30%. At an 8–10% drawdown, halve your risk. And if you hit a 15% decline or approach your firm’s drawdown limit, stop trading for 24–72 hours to reassess your strategy.

Scaling Funded Accounts with Dynamic Sizing

Dynamic sizing is a strategy that helps traders grow funded accounts by adjusting risk based on market conditions and account performance. Instead of applying a one-size-fits-all approach to every trade, you tailor position sizes to reflect your current situation. This method not only aligns with the strict rules of prop firms but also helps protect your capital during challenging periods. By adapting your risk, you create a solid path for expanding your funded accounts.

Moving from Evaluation to Larger Funded Accounts

Dynamic sizing plays a key role in progressing from initial evaluations to managing multiple funded accounts. Prop firms often impose limits, such as capping a single day’s profit at 40% of total gains [9][7]. Using static position sizing can make it harder to comply with these restrictions. For example, one oversized trade could breach the rules and disqualify you from payouts. Dynamic sizing helps smooth out your equity curve by keeping risk proportional to your account balance, making it easier to meet these requirements.

It’s worth noting that fewer than 1% of participants in some futures prop programs make it to the live-capital stage [10].

"Dynamic risk management takes more patience, but it will keep you trading for longer and it can increase your chances of passing the Funded Account Challenge." – FunderPro [2]

Consistency is crucial. After demonstrating steady performance on a single account for at least three months, you can start scaling to multiple accounts [7]. Firms like Apex Trader Funding allow traders to manage up to 20 active funded accounts per household, while others like Topstep and Tradeify typically limit it to five accounts [7]. When handling accounts of different sizes – say $50,000 and $150,000 – you can use position sizing multipliers (e.g., 0.5x, 1.0x, 1.5x) to maintain consistent percentage risk across your portfolio [7].

Maximizing Payouts with High-Quality Trades

When scaling, it’s essential to focus on high-conviction setups – trades with strong technical alignment. Allocate your full risk to these setups, while reducing risk on marginal ones. For example, you might risk 1% on a high-confidence trade but only 0.5% on a weaker signal [4][1].

This selective approach improves your win rate by filtering out less favorable trades, resulting in a smoother equity curve that aligns with prop firm payout rules. If you’re in a drawdown (down 8% or more), focus exclusively on high-conviction setups and reduce your trade size [3]. This approach helps you avoid compounding losses while staying engaged with the market.

Scaling across multiple accounts amplifies your earning potential. For instance, trading 10 accounts with a 2% monthly return can increase your income from $900 (on a single $50,000 account) to $9,000 for the same effort [7]. The key is sticking to a proven strategy rather than experimenting with new methods. Once you manage more than three accounts, using one of the best trade copying platforms can streamline execution and prevent delays [7].

Managing Drawdowns and Protecting Capital

As you scale up, managing drawdowns becomes even more critical. Drawdowns are inevitable, but how you handle them determines your long-term success. This is where your drawdown ladder – a pre-planned system for reducing risk – comes into play.

"Drawdown isn’t caused by losing trades – it’s caused by not adjusting position size when market conditions change." – Issam Kassas [3]

Here’s why this matters: if you’re trading 10 accounts, a drawdown violation on one account only impacts 10% of your total capital access, not 100% [7]. Diversifying across multiple prop firms, such as Apex, Take Profit Trader, and Tradeify, also protects you from risks like platform outages or unexpected rule changes [7].

Some firms even offer built-in scaling mechanisms. For example, Topstep has a Dynamic Risk Expansion system that allows traders to scale up to 100 lots and a $100,000 Daily Loss Limit after reaching $1,000,000 in profit [11]. On a $150,000 account, you start with a $4,500 Daily Loss Limit, which increases to $5,000 after achieving $15,000 in net profit over 10 active trading days [11].

Tools and Resources for Dynamic Sizing

Dynamic sizing works best when backed by tools that ensure precision and consistency. Instead of relying on guesswork, you can use specific indicators and calculators to adjust your risk based on market behavior and the rules set by prop firms.

Using ATR and R-Multiples

The Average True Range (ATR) is a key metric for volatility-based sizing. It calculates the average price movement over a specific period, typically 14 days. When the ATR rises above its 6-month median, it signals increased market volatility. In such cases, reducing position sizes helps maintain consistent dollar risk [1].

For instance, if you’re risking $100 and 2× ATR equals 10 points at $5 per point, your position size would be 2 contracts.

R-Multiples are another crucial tool for assessing trade performance. They compare your profits to your initial risk. For example, if you risk $100 (1R) and earn $300, that’s a 3R win. Tracking R-multiples helps gauge whether your trading strategy is effective enough to scale up or if adjustments are needed [1][4]. Statistically, a trader risking 1% per trade with a 50% win rate would need to lose 69 consecutive trades to cut their account in half [6].

These metrics provide a solid foundation for using prop firm tools to manage risk effectively.

Prop Firm Tools and Calculators

Many prop firms enforce consistency rules, which limit a single day’s profit to 20–40% of total gains [2]. To stay within these limits, tools like the Consistency Rule Calculator on DamnPropFirms can help. By calculating [Best Day Profit] / [Overall Profit] × 100, this tool ensures you avoid disqualification while managing profitable accounts [12].

When facing drawdowns, adjusting your position size is critical. For example:

- At a 5% account drop, reduce your position size by 30%.

- At an 8% drawdown, cut risk by 50%.

- At a 10% loss, stop trading and review your journal.

Some firms, such as Topstep, use trailing drawdowns. In these cases, avoid trades where the required stop-loss exceeds 20% of your live equity buffer [13].

Top Futures Prop Firms for Scaling Accounts

Using these tools and calculators helps align your trading strategy with prop firm rules, making it easier to scale funded accounts. Several firms offer resources tailored for dynamic sizing.

- Tradeify: Provides a built-in trade journal and P&L calendar, enabling you to tag trades and optimize your sizing strategy. As of February 2026, Tradeify has verified payouts surpassing $110 million and offers instant funding with 60-minute automated payouts [14].

- Apex Trader Funding: Offers scalable solutions for traders with consistent results [7].

- Take Profit Trader and Lucid Trading: Both firms provide scaling opportunities, with Lucid Trading offering instant funding to bypass evaluations [15].

- Tradeify: Supports a 1:10 mini-to-micro contract scaling ratio, ideal for fractional risk adjustments [14].

These resources can help you refine your approach and grow your trading account with confidence.

Conclusion

Consistency and Risk Management

Dynamic sizing is what keeps your trading edge alive over the long haul. The gap between traders who barely last a month and those pulling in six figures annually isn’t just about skill – it’s about risk management tailored to funded account setups [16].

"Dynamic position sizing is the operating system underneath every trade you place. Treat volatility as a regime, not an event." – Jasman Mann, International Trading Institute [1]

By adjusting your position sizes based on factors like market volatility, account performance, and drawdown levels, you create a mathematical buffer to weather inevitable losing streaks. This dynamic approach doesn’t just protect your account; it lays the groundwork for sustainable growth [2].

Using Dynamic Sizing to Grow Your Account

Disciplined risk management paired with dynamic sizing opens the door to scalable growth. Start small – master a single account over three months to follow a funded account checklist to establish consistency [7]. Once you’re consistently achieving 2–5% monthly returns, you can begin scaling up to multiple accounts while sticking to the same disciplined methods. For example, firms like Apex Trader Funding allow traders to manage up to 20 funded accounts, while Topstep offers a cap of 5 [7].

FAQs

How do I pick the right risk % per trade for a funded account?

Choosing a risk percentage per trade is all about finding a balance that fits your comfort level. Most traders stick to risking between 0.5% and 2% of their total account on each trade. This range helps limit losses while still allowing room for growth.

However, this isn’t a one-size-fits-all rule. It’s smart to adjust your risk percentage based on two factors: your recent performance and how volatile the market currently is. If you’ve hit a rough patch or the market is especially unpredictable, scaling back your risk can help cushion against losses. On the flip side, during stable periods or when you’re on a winning streak, you might feel comfortable staying closer to the higher end of that range.

The key? Protecting your capital while staying in the game for the long haul.

What’s the easiest way to size positions when ATR suddenly spikes?

When an ATR spike occurs, the simplest approach to position sizing is to account for the heightened volatility. Use the updated ATR value to recalculate your position size. This helps you manage risk effectively and prevents overexposure. By doing so, your trades stay in sync with changing market conditions while keeping risk levels under control.

How should I reduce size after a losing streak without breaking prop firm rules?

Gradually decreasing your position size after a losing streak can be a smart way to manage drawdown while staying within the risk limits set by your prop firm. By using dynamic sizing techniques, you can adjust your trades based on your current account balance and predefined risk parameters. This not only helps you avoid breaking any rules but also ensures your funded account remains protected.