The daily settlement price is the official value of a futures contract at the end of the trading day, calculated by exchanges like CME Group using specific methodologies. It ensures accurate mark-to-market accounting, adjusts open positions, and determines margin requirements. For traders, it influences profits, losses, and compliance with proprietary firm rules like daily loss limits and consistency thresholds.

Key points:

- How it’s calculated: Based on trading activity, such as volume-weighted averages or bid/ask data, during short settlement windows.

- Why it matters: Used for risk management, margin adjustments, and compliance with trading firm policies.

- Tools to use: CME’s Daily Settlements Page for official prices; consistency rule calculators for proprietary trading compliance.

Understanding these processes and using the right tools can help traders align with rules and avoid costly mistakes.

Understanding the "Settlement Price" in Trading and Finance

sbb-itb-46ae61d

Daily Settlement Price Rules

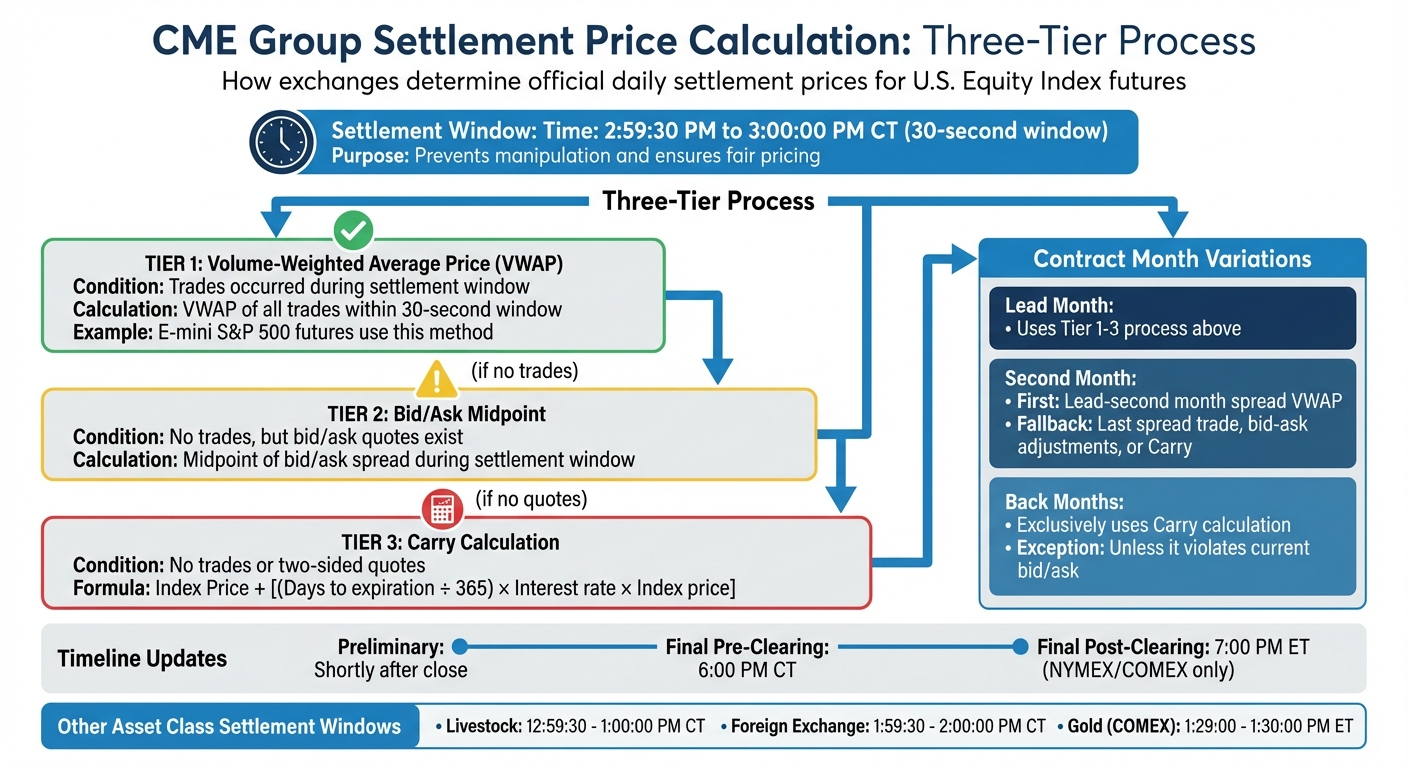

CME Group Three-Tier Settlement Price Calculation Process

Exchanges calculate daily settlement prices using tiered methodologies based on actual trades. These rules are crucial for understanding end-of-day balances and managing margins effectively. For those trading with external capital, understanding these mechanics is a core part of futures prop firm strategies. Knowing how these processes work can help you stay compliant and better manage trading risks.

CME Group Settlement Procedures

CME Group employs a three-tier process to determine settlement prices, tailored by asset class and contract month. For U.S. Equity Index futures, the settlement price is based on trades within a specific 30-second window from 2:59:30 p.m. to 3:00:00 p.m. CT [5].

- Tier 1: The volume-weighted average price (VWAP) of all trades during this window sets the settlement price. For example, E-mini S&P 500 futures rely on this VWAP calculation.

- Tier 2: If no trades occur, the midpoint of the bid/ask spread during the same window is used.

- Tier 3: If no trades or two-sided quotes exist, a "Carry" calculation is applied:

Index Price + [(Days to expiration / 365) × Interest rate × Index price].

For second-month contracts, settlement starts with the lead month-second month spread VWAP. If unavailable, it defaults to the last spread trade, bid-ask adjustments, or the Carry calculation. For back-month contracts (all remaining expirations), the Carry calculation is used exclusively, unless it violates the current bid or ask for those contracts.

Settlement windows differ across asset classes. For instance:

- Livestock contracts settle between 12:59:30 and 1:00:00 p.m. CT.

- Foreign Exchange uses 1:59:30 to 2:00:00 p.m. CT.

- Gold on COMEX settles from 1:29:00 to 1:30:00 p.m. ET [5].

These short windows help prevent manipulation. CME also provides preliminary settlement prices shortly after the close, which are updated until the "Final Pre-Clearing" price at 6:00 p.m. CT. For NYMEX and COMEX products, a third "Final Post-Clearing" run incorporates updated open interest data [4].

Other exchanges, like ICE, implement similar detailed procedures to maintain market integrity.

ICE and Other Exchange Settlement Rules

ICE uses Trade at Settlement (TAS) spreads, allowing traders to place orders tied to the pending settlement price. This approach is common in energy markets, where traders aim to match the official settlement price while avoiding slippage during the closing period.

For back-month contracts with no trading activity, ICE relies on spread relationships to the lead month or prior-day adjustments to determine a fair settlement price [4]. Contracts with zero volume or open interest are marked "for reference only", as they aren’t based on live market activity [4].

Other exchanges have their own unique settlement windows. For example:

- The Moscow Exchange (MOEX) calculates RTS Index settlement prices over a full hour from 3:00 p.m. to 4:00 p.m., a longer period compared to CME’s 30-second window [5].

- Taiwan Futures Exchange (TAIFEX) follows its own region-specific procedures aligned with local trading hours.

Each exchange’s approach reflects its effort to ensure accurate and fair settlement practices tailored to its market dynamics.

Why Daily Settlement Matters for Prop Traders

Daily settlement prices are crucial for determining your official profit or loss at the end of each trading session through mark-to-market accounting [1][3]. These prices serve as the definitive measure of a trader’s performance, directly influencing compliance and strategy decisions in proprietary trading.

Prop firms rely on settlement prices to recalculate account equity daily. A sharp move in settlement prices can trigger your daily loss limit or drawdown, even if you haven’t closed a trade [3][6]. For instance, imagine holding E-mini S&P 500 futures overnight, and the settlement price drops significantly. Your account could breach its drawdown limit before the next trading day starts. Additionally, settlement prices determine margin requirements for overnight positions and set benchmarks for next-day price limits [3][6][7].

Settlement prices also play a key role in consistency rules. For example, the Alpha Futures consistency rule dictates how daily profits impact your maximum withdrawal amount. Many futures prop firms impose limits to ensure that no single trading day accounts for an excessive percentage of total profits – 30% at firms like Phidias, or as low as 20% at stricter firms [2]. These rules rely on end-of-day account balances, which are directly tied to settlement prices. A sudden change in settlement values could inadvertently push traders over these limits.

"Think of it as a risk management tool that rewards steady, repeatable performance over gambling behavior" – Phidias [2]

To help traders stay within these thresholds, tools like the Consistency Rule Calculator from DamnPropFirms provide real-time monitoring. It’s also essential to verify official settlement prices on the CME Group website after market close to ensure compliance with your firm’s rules [1].

For traders aiming to scale up or request payouts, settlement prices determine when equity milestones are met. These milestones might allow you to increase contract sizes or withdraw profits. Since consistency calculations often reset after payouts, you can strategically time withdrawals to "erase" disproportionately large winning days from your record [2]. In the next sections, we’ll cover tools and strategies to help you incorporate settlement price insights into your trading routine.

Tools for Settlement Price Compliance

Ensuring compliance with settlement price rules involves using official data sources and specialized calculators. These tools help verify settlement values, maintain consistency thresholds, and avoid rule violations. By integrating them into your trading routine, you can align official exchange data with your proprietary firm’s requirements.

CME Daily Settlements Page

The CME Daily Settlements Page serves as the go-to source for settlement prices across CME, CBOT, NYMEX, and COMEX products. These prices reflect the fair market value used for marking positions to market [1]. The page provides both preliminary and final settlement prices, with final figures typically available by 6:00 P.M. CT for most CME products.

Preliminary updates occur throughout the afternoon. For instance:

- Equity Index products: Updates at 3:30, 3:45, 4:00, 4:30, and 5:00 P.M. CT.

- Commodity products: Updates begin at 1:30 P.M. CT.

Meanwhile, NYMEX and COMEX products go through three settlement runs – Preliminary, Final Pre-Clearing, and Final Post-Clearing – with the final prices posted by 7:00 P.M. ET [4].

For instruments with low trading volumes or back-month contracts, settlement prices may appear in the "Settle" column on the CME website, even if not listed on the Market Data Platform. This feature is especially helpful for traders managing spreads across multiple contract months [4].

Prop Firm Consistency Rule Calculators

Consistency rule calculators are essential for monitoring whether a single trading day exceeds the allowed percentage of your total profits. A popular option is the Consistency Rule Calculator from DamnPropFirms, which is free to use. This tool allows traders to input daily profits and check compliance before requesting payouts [8]. Most proprietary firms set thresholds between 20% and 40%, with 30% being the most common limit [8].

"The consistency rule is designed to ensure that traders aren’t relying on a single lucky day to meet their profit target. Instead, firms want to see that your profits are distributed across multiple trading days." – ThePropFirmGuide [8]

These calculators typically offer two modes:

- Consistency + Profit Target: Used by firms like Apex Trader Funding.

- Consistency Only: Used by firms like FundedNext Futures.

The mode you choose directly impacts your maximum allowable daily gain, so it’s crucial to confirm your firm’s specific requirements. When entering data, remember to include losing days as negative values since they affect the total net profit used in the calculation.

Custom Spread Calculators

For traders working with back-month contracts or multi-leg strategies, custom spread calculators are invaluable. These tools calculate settlement prices for complex positions like calendar spreads, where certain settlement prices might only be available on the CME Daily Settlements Page and not through standard data feeds [4].

How to Use Settlement Tools in Your Trading Routine

Using Settlement Tools After Market Close

After the market closes, it’s crucial to verify settlement prices to confirm your positions and margin requirements. The key moment comes when CME Clearing publishes the final settlement prices, typically after 5:30 P.M. CT. These official prices play a vital role in determining your profit or loss and margin obligations. Start by checking the CME Daily Settlements page to review benchmark prices for all your positions.

Keep in mind that settlement times differ depending on the asset class – a detail covered in the earlier section on CME Group Settlement Procedures.

"The final settlement price is the official daily settlement published by CME Clearing and is used in pay/collects and margin calculations."

– CME Group [9]

To ensure accuracy, cross-check intraday settlement data with the official prices after 5:30 P.M. CT. This two-step process helps you identify potential issues early while making sure your records align with the clearinghouse’s calculations. First, use intraday data to anticipate any drawdowns. Then, finalize your verification with the official settlement data. This method not only protects your margin calculations but also ensures your trading setup remains compliant with your firm’s current policies [9].

Staying Updated with Prop Firm Rules

Prop firms often make adjustments to their rules, such as changing consistency thresholds, tweaking trailing drawdown mechanics, or modifying payout structures. These updates can happen with minimal notice, so it’s important to stay informed. Before placing trades, take time to review your firm’s payout policies and drawdown mechanics to avoid any accidental violations, especially during periods of high market volatility.

"Before you start trading, understand the payout rules and trailing drawdown mechanics."

– Alexander, Verified Trader, Clever Daytrading [10]

Be particularly vigilant during weekends and holidays, as firms sometimes announce significant rule changes during these times. For instance, firms like Apex Trader Funding have implemented updates effective March 2026. To stay informed, consult review pages like DamnPropFirms, which cover firms such as Take Profit Trader, FundedNext Futures, Alpha Futures, Tradeify, Lucid Trading, Purdia, and Topstep.

Common Mistakes and Compliance Tips

One of the most frequent missteps traders make is confusing the closing price with the settlement price, assuming the last traded price determines their daily profit and loss. In reality, the settlement price is usually a volume-weighted average calculated over a specific time window. For example, CME Equities use the 30-second period from 2:59:30 P.M. to 3:00:00 P.M. CT to calculate this price [3]. Misunderstanding this distinction can lead to errors in margin calculations.

Another challenge arises with contract-specific nuances, particularly when it comes to back-month settlement adjustments. If you hold contracts beyond the front month, clearing houses often calculate settlement prices based on spread relationships with other contract months, rather than the last traded price [12]. On volatile trading days, settlements might even rely on the prior day’s price differential. Failing to account for these adjustments can result in an unexpected settlement price, potentially causing an immediate violation of your daily loss limit – even if you haven’t closed a single losing trade [13].

Over-leveraging is another common pitfall. Many traders size their positions based on the minimum margin requirement instead of considering their actual account size and risk tolerance. This approach can be risky because leverage magnifies both gains and losses based on the full value of the contract – not just the margin deposit [11]. Without a buffer for settlement-driven unrealized losses, you may inadvertently breach your daily loss limit, as most futures prop firms factor these unrealized losses into their calculations [13].

Lastly, consistency rule violations are a frequent compliance issue for proprietary traders. For example, if a single profitable day accounts for more than 30% of your total profits, you won’t necessarily fail your account. However, payout requests will be restricted until you dilute this ratio through more consistent trading [2]. At firms like Phidias, the threshold is 30%, while others may enforce stricter limits, such as 20% [2]. To address this, you can calculate your new profit target using the formula: Best Day Profit ÷ 0.30 = New Profit Target [2]. This highlights the importance of pairing strong risk management with adherence to technical compliance.

Conclusion

Daily settlement rules play a key role in ensuring compliance, calculating margin obligations, and tracking profits and losses, all while maintaining consistent trading practices. As Phidias Prop Firm puts it:

"Steady profits indicate a proven trading system, not luck. This rule is not designed to fail you. It’s designed to encourage the trading habits that lead to long-term success" [2].

Using the right tools can make compliance much easier. For instance, the CME Daily Settlements page offers official settlement data, and consistency rule calculators help ensure that no single day surpasses your firm’s threshold [8]. These tools minimize manual errors and help avoid payout denials caused by overlooked violations.

Staying informed about changing regulations is equally important. Prop firms like Apex Trader Funding have recently adjusted their account structures and consistency rules. Before requesting a withdrawal, double-check your metrics with a calculator and consult your firm’s latest rulebook to ensure everything is in order.

FAQs

Why is my P&L different from the last traded close?

Your profit and loss (P&L) might not match the last traded close because the settlement price – used to mark positions daily – is calculated differently. Instead of relying on the last traded price, it’s based on an average of prices over a specific time frame. This approach is designed to reflect the fair market value more accurately and supports precise risk management. Differences can also result from unique exchange calculations or unusual market activity during the settlement period.

When do settlements become final, and which one counts for margins?

At the end of each trading day, settlements are considered final. The settlement price – used to calculate margins – is determined by the exchange. This price reflects the fair market value based on trading activity during the market’s closing period.

How can settlement prices trigger prop firm drawdowns on open trades?

Settlement prices play a key role in how prop firms handle drawdowns, as they directly impact account equity or balance when open trades lose value. If these prices lead to losses that exceed a firm’s drawdown limits, traders might face penalties or even account closure. This becomes particularly challenging for firms that factor in both open trade values and end-of-day account balances when calculating drawdowns, as floating losses can also push traders into violation territory.