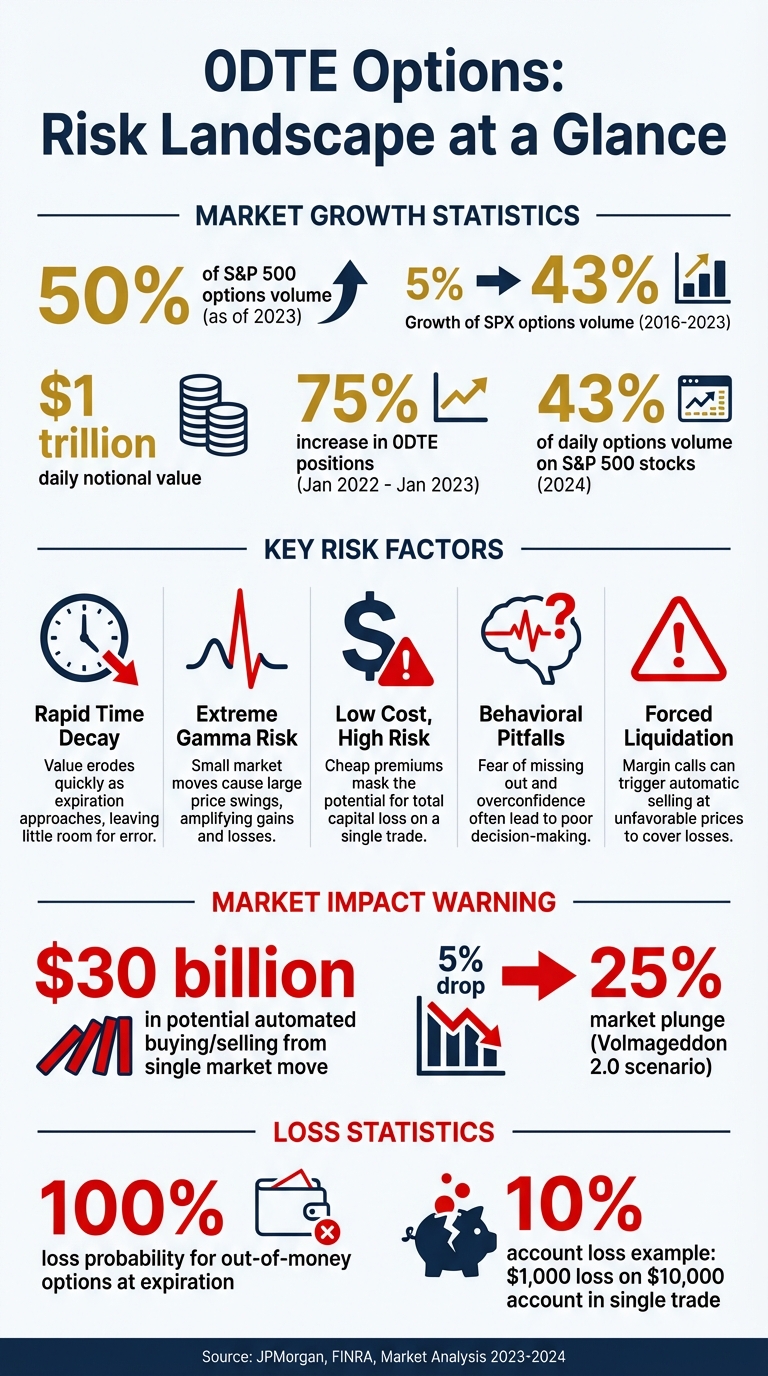

Zero DTE (zero days to expiration) options have exploded in popularity, now making up nearly 50% of S&P 500 options volume as of 2023. These contracts, expiring the same day they’re traded, offer traders the allure of quick profits but carry steep risks. Here’s what you need to know:

- Rapid Time Decay: The value of these options erodes quickly throughout the trading day, leaving little room for error.

- Extreme Volatility: Even small price moves in the underlying asset can cause massive swings in the option’s value, thanks to heightened gamma sensitivity.

- Low Cost, High Risk: While priced cheaply, these options often mislead traders into taking oversized positions, leading to significant losses.

- Behavioral Pitfalls: Emotional trading, poor risk management, and late-day volatility amplify the dangers.

- Individual Stock Risks: Newer daily expirations for single stocks add company-specific risks, such as sudden news-driven price spikes.

Despite their appeal, traders often underestimate the complexity and risks of 0DTE options. Without strict discipline and risk management, these contracts can quickly wipe out accounts. Dive deeper to understand the structural risks, trading behaviors, and why these options are not for everyone.

Zero DTE Options Risk Factors and Market Impact Statistics

What Are Zero Day Options? (0DTE Explained)

sbb-itb-46ae61d

What Are Zero DTE Options

Zero days to expiration (0DTE) options are contracts that expire on the same trading day. Unlike traditional options, which allow traders days, weeks, or even months to see their strategies unfold, 0DTE options pack everything into a single trading session. The contract’s value diminishes at a rapid pace as the day progresses, making them an extremely time-sensitive tool. This compressed timeline amplifies both the potential rewards and the risks, as we’ll explore in the coming sections.

How Zero DTE Options Work

At their core, 0DTE options function like standard options, with their value influenced by the underlying asset’s price, volatility, and the relentless impact of time decay (theta). However, because these options are so close to expiration, their behavior becomes particularly volatile. This heightened sensitivity, known as gamma risk, can lead to dramatic swings in value. For example, even a slight movement in a major index like the S&P 500 or a high-volatility stock can cause a 0DTE option’s price to skyrocket – or plummet – within moments.

Traders are drawn to 0DTE options for a few key reasons. First, they eliminate overnight risk, meaning there’s no worry about price gaps when the market is closed. Second, they enable rapid capital turnover, as funds are only tied up for a few hours instead of days or weeks [2][5]. For sellers, the appeal lies in the rapid erosion of premium throughout the trading day, creating opportunities to profit from this decay. However, this same volatility and time pressure can lead to risky trading practices, which we’ll dive into shortly.

Why Low Premiums Create False Confidence

One of the most striking features of 0DTE options is their low cost. Since there’s virtually no time value left, these contracts are often priced at just a few cents, compared to the higher costs of longer-term options [9]. While this affordability might seem like a low-risk way to trade, it can create a dangerous illusion of safety. Many retail traders treat these contracts as “lottery tickets,” assuming the small upfront cost minimizes their risk. In reality, if the option doesn’t move into the money by the end of the trading day, the likelihood of a total loss is almost guaranteed [2][10].

"A novice trying to get rich fast without doing their homework could be left nursing a really nasty loss." – Investopedia [2]

This low cost often tempts traders into taking on oversized positions. When contracts are priced at just a few cents, it’s easy to buy far more than is financially prudent. However, even a small unfavorable market move can result in a 100% loss within hours [9][10]. On the flip side, sellers might be drawn to the rapid premium decay, but an uncovered position can lead to unlimited losses if the market moves sharply against them [2][9]. These dynamics highlight the inherent risks and challenges of trading 0DTE options, which we’ll examine further in the discussion on structural risks.

Structural Risks of Zero DTE Options

Zero DTE (0DTE) options, which expire on the same day they are traded, come with a unique set of risks. Unlike longer-dated options, these contracts operate within a compressed timeframe that not only limits opportunities but also fundamentally alters their behavior. Grasping these risks is essential for anyone considering trading them.

Time Decay Acceleration

In 0DTE options, theta decay – the loss of an option’s value as time passes – accelerates dramatically as the market approaches its 4:00 PM ET close [2][10]. With each passing hour, the extrinsic value of these options erodes rapidly. For buyers, this means there’s a very narrow window to profit; if the expected directional move doesn’t happen quickly, theta decay can wipe out potential gains [9][10].

While some traders take advantage of this rapid decay, the strategy is not without peril. The extreme time sensitivity means they’re also exposed to sudden, sharp price movements as expiration nears. Recent data shows that 0DTE options now make up nearly half of SPX trading volume [1][6]. This surge in popularity underscores the appeal of quick theta decay but also highlights the risks that come with it. As the clock ticks down, these options become highly sensitive to price changes, creating what’s known as gamma-driven price swings.

Gamma Risk and Delta Swings

Gamma measures how quickly an option’s delta – its sensitivity to price changes in the underlying asset – shifts. For 0DTE options, gamma reaches extreme levels as expiration approaches [6][9]. This means the delta of an option can swing wildly between 0 (worthless) and 1.00 (fully in the money) if the underlying asset hovers near the strike price. Even small market movements can lead to outsized profit-and-loss (PnL) swings [6].

"At expiration, an option is either in the money or out of the money – with absolute certainty. (In option terms, its delta is either 0 or 1.00.) If the market vacillates above and below a strike on expiration day, so does its delta. That change in delta is called gamma, and it represents uncertainty." – Britannica Money [6]

For example, on December 18, 2024, the S&P 500 dropped nearly 3% during the final two hours of trading after Federal Reserve Chair Jerome Powell announced future rate cuts. This was the steepest FOMC announcement-day decline since March 2020. Many 0DTE traders using neutral strategies like iron condors suffered maximum losses as the index moved sharply through their short strikes [9]. In such a high-gamma environment, what started as a controlled position quickly turned catastrophic. This highlights how even minor price fluctuations can spiral into significant losses, a phenomenon explored further below.

How Small Price Moves Create Large Losses

With almost no time value left, 0DTE options are driven almost entirely by their intrinsic value. This means any small movement in the underlying asset is reflected immediately and dramatically in the option’s premium. A seemingly insignificant price change can transform potential gains into a total loss, illustrating the nonlinear risk tied to these contracts.

According to analysts at JPMorgan, a substantial intraday market move could spark as much as $30 billion in automated buying or selling tied to 0DTE positions [1][3]. In volatile markets, this can force market makers to rapidly adjust their hedges. Such collective hedging activity can amplify the very price swings that triggered the adjustments in the first place. Marko Kolanovic, JPMorgan’s Chief Global Market Strategist, has even warned of a potential "Volmageddon 2.0" scenario. In this theoretical event, 0DTE-driven volatility could escalate a standard 5% intraday drop in the S&P 500 into a catastrophic 25% market plunge [3][11]. While this remains hypothetical, it underscores just how quickly small price moves can snowball into massive losses when gamma risk is at its peak.

Why Traders Lose Money with Zero DTE Options

Grasping the structural risks of zero-day-to-expiration (0DTE) options is one thing. But steering clear of the behavioral pitfalls that turn those risks into losses? That’s a whole different challenge. Even traders who understand the mechanics of gamma and theta often sabotage themselves with predictable mistakes. Let’s break down some of the key missteps that lead to losses.

Position Sizing Errors

The low cost of 0DTE options can create a deceptive sense of safety, luring traders into oversized positions. Kirk Du Plessis, Founder of Option Alpha, highlights the importance of restraint:

"All of my personal trades in SPX so far have been trades with ~$500 of risk or less precisely because I want to keep position sizes small" [7].

But many traders don’t follow this approach. Between January 2022 and January 2023, 0DTE positions surged by 75% [5], often driven by lottery-style bets [2]. Here’s the harsh reality: even small losses can quickly drain a modest account. For example, if you have $10,000 and buy 20 contracts at $50 each, you’re risking $1,000. If those options expire worthless – a common outcome – you lose 10% of your account in just one trade [10].

Adding to the risk, brokers often liquidate 0DTE positions before the market closes if there’s not enough capital to cover potential assignments. This forced liquidation typically happens at unfavorable prices, locking in losses even if the trade might have recovered later.

Trading Late-Day Volatility

The final hour of trading is where 0DTE options become particularly treacherous. As the market nears its close, theta decay accelerates sharply, and gamma risk reaches its peak [2][8]. Price movements that might seem minor earlier in the day can cause wild swings in option prices late in the session.

Take August 15, 2023, for example. Between 3:00 PM and 3:30 PM, the SPX index dropped 0.4%, slipping from 4,451 to 4,433. During this time, the 4,440-strike put saw enormous activity – over 100,000 contracts traded. By 3:30 PM, market makers shifted from long gamma to short gamma [4]. Traders entering positions during this chaotic window faced rapid decay and worsening liquidity [7].

The pressure to see immediate results in such a short time frame often leads to poor decision-making. As Investopedia points out:

"At this late stage, time is of the essence… something that seemed certain in the morning may end up backfiring in the afternoon" [2].

This time crunch and increased risk often push traders into emotional, rather than rational, decisions.

Emotional Trading After Losses

The all-or-nothing nature of 0DTE options fuels impulsive behavior. A small loss can trigger a desperate attempt to recover before the market closes, leading traders to double down on risky positions as time runs out.

This setup fosters a gambling mindset rather than a disciplined trading approach. As NerdWallet explains:

"Zero-day options traders are making everything-or-nothing bets on expiration day. That means 100% losses are harder to avoid" [10].

Quick wins can create a dopamine-fueled cycle, tempting traders to abandon stop-loss orders or exit strategies. Instead, they hold onto losing positions until panic forces them to sell. In the high-gamma environment of 0DTE options, a trade can swing from profit to total loss within minutes, leaving traders scrambling [1][3]. By the market’s close, what started as a small setback can snowball into a significant loss, wiping out gains from the entire day – or even the week.

Psychological Dangers of Zero DTE Trading

Zero Days to Expiration (0DTE) trading doesn’t just come with structural risks – it also creates a psychological battleground that challenges even the most disciplined traders. The fast-paced nature of these trades, combined with extreme time pressure, reshapes decision-making in ways that can quickly drain capital.

Reward Response and Overtrading

The immediate feedback loop of 0DTE trading triggers a dopamine surge similar to what gamblers experience. This creates a psychological cycle that encourages compulsive trading behavior.

The appeal lies in the promise of "fast results" and the allure of a "lotto trade" mentality, rather than in sound strategies [2][10]. The low cost of entry only fuels this behavior, making repeated trades seem reasonable – even when they aren’t. As John Manley from DMS puts it:

"The ultra-short-term nature of 0DTE makes engagement almost a binary event – money can be made and lost very quickly depending on the intraday movement of a stock or index" [6].

This all-or-nothing dynamic, where trades either deliver significant profits or expire worthless, resembles lottery tickets more than calculated investing. By 2024, 0DTE options made up over 43% of the daily options volume on S&P 500 stocks [10]. The introduction of daily expirations in 2022 enabled traders to engage every single business day, making it harder to resist the temptation to overtrade [6][10].

Adding to the chaos is gamma-induced volatility, which causes dramatic swings in profit and loss throughout the day. A position can move from profit to loss – and back again – multiple times before expiration [6]. These rapid fluctuations are often described as "unnerving" [6], pushing traders to act impulsively. Whether it’s locking in gains before they disappear or chasing losses, this constant pressure feeds into risky trading habits and erodes discipline.

Loss of Trading Discipline

Time pressure is a stealthy destroyer of trading discipline. With less than 24 hours – sometimes only a few hours – to make the right moves, patience often goes out the window. The narrow window for action forces traders into split-second decisions [2], and under this stress, even the best-laid plans can unravel.

As expiration nears, theta decay accelerates sharply, and the gamma-driven volatility makes positions hypersensitive to small price changes [6]. This environment of rapid option decay and high-gamma swings undermines risk management, leading traders to abandon stop-loss orders, hold onto losing positions for too long, or exit winning trades prematurely. As Investopedia warns:

"A novice trying to get rich fast without doing their homework could be left nursing a really nasty loss" [2].

Adding to the problem is the false sense of safety from low premiums. Contracts priced at $20 or $50 may seem cheap, but as NerdWallet notes:

"Zero-day options traders are making everything-or-nothing bets on expiration day. That means 100% losses are harder to avoid" [10].

This all-or-nothing structure means even minor mistakes can lead to complete capital loss. And because these losses happen so quickly, there’s often no time to reflect or adjust before the next trade. The daily notional value of 0DTE trading has reached around $1 trillion [1], showing how normalized this cycle of rapid wins and losses has become – even though it systematically undermines discipline and risk management.

Zero DTE Options on Individual Stocks

The availability of zero DTE (days-to-expiration) options has expanded beyond major indexes like the S&P 500 to include single-stock options with daily expirations on popular equities. While index options spread risk across a broader market, single-stock zero DTE contracts focus that risk on a single company, making them particularly sensitive to sudden news or events. This shift introduces a new layer of complexity, combining the structural challenges of zero DTE trading with risks unique to individual stocks.

Single-Stock Risk Factors

Individual stocks are subject to idiosyncratic volatility – sharp, unpredictable price movements driven by company-specific news. Unlike indexes, where broader market trends often smooth out volatility, single-stock options can experience abrupt price gaps that leap over strike prices before traders have a chance to react. Between January 2022 and January 2023, retail participation in zero DTE contracts surged by roughly 75% [5], much of it fueled by speculative trading on individual stocks. This amplifies the already high-risk profile of zero DTE options, exposing traders to sudden losses tied to company-specific developments.

Adding to the risk is the settlement process. Unlike index options that settle in cash, single-stock options are physically settled and follow the American-style exercise model. This means traders face the possibility of forced assignment if their accounts lack the necessary funds or shares to meet the contract’s obligations [6][7]. Brokerages are quick to act in such cases. As FINRA explains:

"For options that are physically settled… your firm may liquidate the position prior to the close of trading if you don’t have the required funds or shares of the underlying security to meet the potential purchase or delivery obligation" [5].

This forced liquidation often occurs at unfavorable prices, cutting off potential gains or locking in losses before traders can respond.

Early Liquidity Problems

Liquidity challenges only add to the complexity of trading single-stock zero DTE options. These contracts often suffer from thin order books and wide bid-ask spreads compared to their index counterparts. Kirk Du Plessis, founder of Option Alpha, highlights this issue:

"I have found that sometimes certain strikes just don’t have the same liquidity as others… it’s sometimes difficult to execute trades at favorable prices and can increase slippage" [7].

As trading progresses throughout the day, liquidity can shift away from certain strikes, leaving traders stuck in positions they can’t easily exit without incurring steep losses. While SPX zero DTE options accounted for over 47% of total SPX volume in 2024 [7], single-stock options lack this level of participation. The combination of high gamma sensitivity and poor liquidity creates a volatile environment where option prices can swing dramatically, making it extremely challenging to manage risk effectively as expiration nears.

These liquidity issues further emphasize the importance of disciplined risk management, especially in the fast-moving world of zero DTE trading.

Zero DTE Options vs Futures Trading Risk

Futures trading tends to offer more predictable, linear risk, while zero DTE options come with nonlinear risks that can escalate quickly and unpredictably.

Nonlinear vs. Linear Risk Profiles

Futures contracts operate with a linear risk profile. This means that for every point the underlying asset moves, your profit or loss changes by a fixed amount. For example, if the S&P 500 moves 10 points, the corresponding gain or loss is straightforward and consistent.

Zero DTE options, however, introduce nonlinear risk due to the influence of delta and gamma. These factors make risk assessment more complex and amplify the challenges of limited time for adjustments. Market makers often hedge this risk using futures because the risk behavior in futures remains more predictable and easier to manage [6].

Time Constraints and Position Management

Futures positions allow for flexibility. They can be held and adjusted over days or even weeks, giving traders ample time to recover from adverse market movements. In contrast, zero DTE options must be closed by the end of the trading day to avoid assignment issues. This strict time limit eliminates overnight risk but also removes any opportunity for recovery if a trade moves against you [2].

Differences in Risk Transparency

Another key distinction lies in how transparent the risks are. Futures trading provides clear and constant risk parameters – your exposure only changes when you adjust your position size. Zero DTE options, on the other hand, lack this clarity. As prices approach the strike, the option’s delta can shift dramatically, often leading to near-binary outcomes. This unpredictability makes managing risk significantly harder [6].

For traders looking for a more structured way to manage risk, platforms like Apex Trader Funding and Take Profit Trader enforce strict drawdown rules in futures trading. These rules help protect accounts from the rapid losses often associated with zero DTE options. If controlled risk is your priority, futures trading offers a more consistent and manageable framework compared to the volatile nature of zero DTE options.

Who Should Not Trade Zero DTE Options

High-Risk Trader Categories

Zero DTE options trading isn’t for everyone. These trades require a solid understanding of the market and a disciplined approach – qualities that many traders, especially beginners, may not yet have. For novice traders, the compressed timeframe of zero DTE options leaves little room for error. A single mistake can lead to significant losses, and there’s no time to recover or learn on the go.

Traders with smaller accounts, particularly those with less than $25,000, face additional hurdles due to the Pattern Day Trader (PDT) rule. Since zero DTE trades are opened and closed within the same day, making four or more day trades in a five-business-day period could result in account restrictions [9].

Emotion-driven traders also face challenges with zero DTE options. The fast-paced nature of these trades often leads to impulsive decisions rather than well-thought-out strategies [2].

Uncovered option sellers are another group that should tread carefully. A sudden market move can lead to losses far exceeding the premium they initially received [9]. Without proper risk management, these vulnerabilities can quickly drain an account.

How Accounts Get Wiped Out

The risks of zero DTE trading don’t stop at small, cumulative losses. A single oversized bet, often the result of poor risk management, can wipe out an account entirely. This risk is compounded by the possibility of forced liquidation. If a trader doesn’t have enough funds to handle a potential assignment, brokers may step in and liquidate positions before the market closes – often at prices that work against the trader. As FINRA warns:

"If your firm opts to liquidate your option position prior to the close of trading, your firm may place an order for you at a price that might limit potential profits or even lead to potential losses." [5]

The combination of rapid time decay and sharp price swings, often referred to as "gamma whipsaws", creates a tough environment for traders. Those with smaller accounts are particularly at risk, as PDT restrictions can prevent them from exiting positions when needed [9].

Final Assessment of Zero DTE Options Risk

Main Risk Points

Zero DTE (zero days to expiration) options come with a high level of risk. From 2016 to 2023, the portion of SPX options volume tied to 0DTE trading skyrocketed from 5% to 43%, with the daily notional value hitting nearly $1 trillion[6][1]. Despite this incredible growth, the risks tied to these trades remain as significant as ever.

The primary dangers include rapid time decay, sharp gamma-driven delta shifts, and the possibility of forced liquidation before the market closes[5]. When 0DTE options are applied to individual stocks, the risks grow even larger due to the unpredictable nature of company-specific events.

JPMorgan analysts have estimated that a major market movement could set off about $30 billion in automated buying or selling of 0DTE positions[1][3]. Marko Kolanovic, Chief Global Markets Strategist at J.P. Morgan Chase, highlighted this risk:

"The growing size of the 0DTE segment may lead to sharp market swings as large as $30 billion, particularly in the current low liquidity environment"[12].

These risks make it clear that a disciplined and well-thought-out approach is critical for anyone engaging in 0DTE trading.

Focus on Sustainable Trading

The fast-paced nature of 0DTE trading often leads to quick losses, especially for traders who lack a structured strategy. Many underestimate how small, frequent losses can add up over time, potentially eroding their capital at a rapid rate. Even defined-risk strategies can fail to prevent significant losses if not managed properly.

Futures prop trading firms offer an alternative by providing defined risk parameters and strict oversight. Firms like Apex Trader Funding, Take Profit Trader, and Topstep implement strict drawdown limits and position sizing rules. These measures help traders avoid oversized positions and excessive trading. Futures trading also allows for more effective risk management and recovery strategies. At DamnPropFirms, the focus is on preserving capital and maintaining structured risk control rather than chasing quick, short-term gains.

FAQs

What are the main risks of trading zero DTE options?

Trading zero DTE (zero days to expiration) options is not for the faint of heart. These contracts are highly sensitive to even the smallest market fluctuations, which can lead to dramatic swings in both profits and losses. As expiration nears, time decay kicks into overdrive, quickly eating away at the option’s value if the market doesn’t move in your favor. On top of that, gamma risk – the rapid shift in delta – can create sudden and unpredictable losses, making these trades incredibly volatile.

There’s also a psychological element that can amplify the risks. The relatively low premiums often tempt traders to take on oversized positions, while the fast-paced nature of these options can lead to chasing late-session volatility. Emotional decisions, like revenge trading or treating these contracts as lottery tickets, can be disastrous, potentially wiping out entire accounts. The introduction of zero DTE options for single stocks, particularly volatile tech names, adds yet another layer of risk. Factors like unexpected earnings results or breaking news can turn these trades into a minefield. While the potential for quick gains exists, success demands strict discipline and a solid risk management strategy to avoid catastrophic losses.

What is gamma risk, and how does it affect zero DTE options?

Gamma risk is all about how quickly and unpredictably delta can change as the price of the underlying asset moves. When it comes to zero DTE (day-to-expiration) options, even small price shifts can lead to sudden and dramatic changes in value.

Since zero DTE options expire so quickly, gamma risk becomes even more intense. This makes it challenging for traders to keep their positions under control. The heightened sensitivity can lead to rapid profits or losses, adding an extra layer of risk to these trades.

Why are zero DTE options considered unsuitable for beginner traders?

Zero DTE options aren’t the best starting point for beginner traders. Why? Because they come with high risk and require a solid grasp of how the market works. Since these options expire the same day they’re bought, there’s almost no time to fix mistakes, recover losses, or adjust positions if the market takes an unexpected turn.

For newcomers, the fast-moving nature of these trades can be overwhelming. It often leads to emotional reactions like revenge trading or taking on positions that are too large. Without experience and a strong focus on managing risk, these trades can drain an account faster than expected, making them a risky choice for those just starting out.