When futures contracts expire, they can settle in two ways: cash settlement or physical delivery. Here’s the difference:

- Cash Settlement: No physical transfer of goods. Traders settle by paying or receiving the price difference in cash. Common for financial instruments like stock indices. Lower margin requirements (~5%), simpler process, but no ownership of the actual commodity.

- Physical Delivery: The actual asset (e.g., gold, crude oil, wheat) is delivered to the buyer. Often used by industries needing raw materials. Higher margin requirements (~10%), added costs (storage, transport), and logistical complexity.

Key Takeaway: Cash settlement is suitable for speculators and traders focused on price movements, while physical delivery works best for businesses needing the actual commodity. Choose based on your trading goals and risk tolerance.

| Feature | Cash Settlement | Physical Delivery |

|---|---|---|

| Core Mechanism | Financial exchange | Actual asset transfer |

| Margin Requirement | Lower (~5%) | Higher (~10%) |

| Users | Speculators, traders | Producers, manufacturers |

| Complexity | Simple | Complex logistics |

Cash Settlement vs Physical Delivery in Futures Trading Comparison

Physical Delivery VS Cash Settlement: Futures Discovery EP 7

sbb-itb-46ae61d

What Is Cash Settlement?

Cash settlement is a way to wrap up futures contracts with a monetary exchange instead of physically delivering the underlying asset. When the contract expires, the exchange determines a final price, and traders settle the difference in cash – no goods are exchanged. This method simplifies the process, which is why many top futures prop firms prefer cash-settled instruments for their traders.

This approach is especially common for financial instruments like stock index futures. For instance, S&P 500 futures use cash settlement because delivering an actual basket of 500 stocks would be logistically overwhelming.

How Cash Settlement Works

The process kicks off by establishing a final settlement price. Exchanges often rely on a volume-weighted average price (VWAP), which factors in trading volume to calculate an average price for the underlying asset during a set time period. For certain commodities, Price Reporting Agencies like Fastmarkets gather data on cash transactions, bids, and offers to create price assessments.

Take January 2025 as an example: CME Group settled Southern Yellow Pine (SYP) futures by averaging daily Fastmarkets assessments from January 2 ($414.00) through January 15 ($435.00). This calculation produced a final settlement price of $428.40. Once the price is determined, clearinghouses handle the fund transfers between buyers and sellers. For example, if a trader bought a crude oil contract at $70 and it settles at $78, they would earn $8,000 (an $8 difference multiplied by 1,000 barrels). This efficient system highlights the advantages discussed below.

Benefits of Cash Settlement

Cash settlement eliminates the need for storage, insurance, transportation, and quality checks, making it a more straightforward option. Additionally, cash-settled contracts typically require lower margins – around 5% compared to 10% for physical delivery. This lower margin requirement enhances buying power, enabling traders to manage more positions simultaneously.

"Cash settlement is the more popular settlement method for commodities because of the convenience and instantaneity the method offers" – CFI Team

Drawbacks of Cash Settlement

However, cash settlement has its downsides. Traders don’t gain physical ownership, which can be a problem for manufacturers who need the actual product. There’s also the risk of basis discrepancies – when the settlement index doesn’t perfectly align with the physical market price. Furthermore, if Price Reporting Agency assessments are flawed or lack credibility, the final settlement price might not reflect real market conditions.

What Is Physical Delivery?

Physical delivery is a settlement method where the actual asset tied to a futures contract changes hands when the contract expires. Instead of settling the contract with a cash difference, the seller (holding a short position) provides the real commodity – whether that’s gold, crude oil, wheat, or live cattle. This approach creates a direct connection between the futures market and the actual commodity market. It’s a different process compared to cash settlement, which simply involves a payment to reflect price differences.

This method is commonly used by commercial hedgers and industrial buyers. For instance, a meat packer might use live cattle futures to secure their supply, or a grain miller could rely on wheat futures to ensure they have the stock needed for operations.

"In a contract that is physically delivered, the underlying physical market is inherently tied to the futures contract through the delivery mechanism."

– CME Group

Physical delivery requires careful coordination between the buyer, seller, and logistics providers. Contracts outline specific requirements for the commodities. For example, gold must be 99.5% pure and weigh 400 troy ounces, while wheat must meet USDA’s No. 2 hard red winter standard for moisture and protein content. A live cattle futures contract specifies the delivery of 40,000 pounds of cattle. This process tends to be more complex and costly than cash settlement due to added expenses like storage, transportation, insurance, and brokerage fees.

How Physical Delivery Works

Here’s how the process unfolds when a contract nears expiration. The exchange pairs traders holding long positions with those holding short positions. About 30 days before the contract’s last trading day, the seller must issue a delivery notice, detailing the quantity, grade, and approved delivery location of the commodity. A clearing broker or agent organizes the trade: the seller delivers the commodity to an exchange-approved facility – such as a designated grain elevator for agricultural goods or the London Bullion Market for gold. The buyer then pays the full contract value based on the final settlement price, which acts as the invoice price.

Strict rules govern delivery locations and quality standards. If the goods don’t meet contract specifications, they can be rejected or penalized. Most retail traders avoid this process by closing their positions or rolling them over to a later contract month at least 10 days before expiration. This is especially true for those using funded trading accounts through prop firms, where physical delivery is typically prohibited.

Benefits of Physical Delivery

Physical delivery ensures actual ownership of the commodity, which is essential for businesses that depend on raw materials. It also helps align futures prices with the spot market, making these contracts effective tools for hedging. Khalid Ahmed from WallStreetMojo highlights this advantage:

"Physical delivery is important for industries and commercial buyers to gain timely and reliable access to commodities."

For producers and industrial users, physical delivery guarantees the receipt or delivery of the exact grade and quality of the commodity they need, reducing basis risk. While this method secures direct access to the commodity, it does come with its own set of challenges.

Drawbacks of Physical Delivery

The logistical hurdles tied to physical delivery can be significant. Traders must arrange transportation, secure storage, and manage delivery, which makes this method less appealing for speculators who don’t need the physical asset. Additional costs, such as storage fees, insurance, transportation, and brokerage charges, can quickly add up.

Another challenge is reduced liquidity as contracts near expiration, since many traders exit to avoid delivery obligations. This can make it harder to adjust positions or close them at favorable prices. For these reasons, most futures traders opt for cash settlement.

Traders who do hold positions into the delivery month need to maintain a free-margin buffer of at least 30% to cover unexpected price movements and additional costs. Missing the notice deadline or failing to exit in time can result in unwanted delivery obligations, leading to significant expenses.

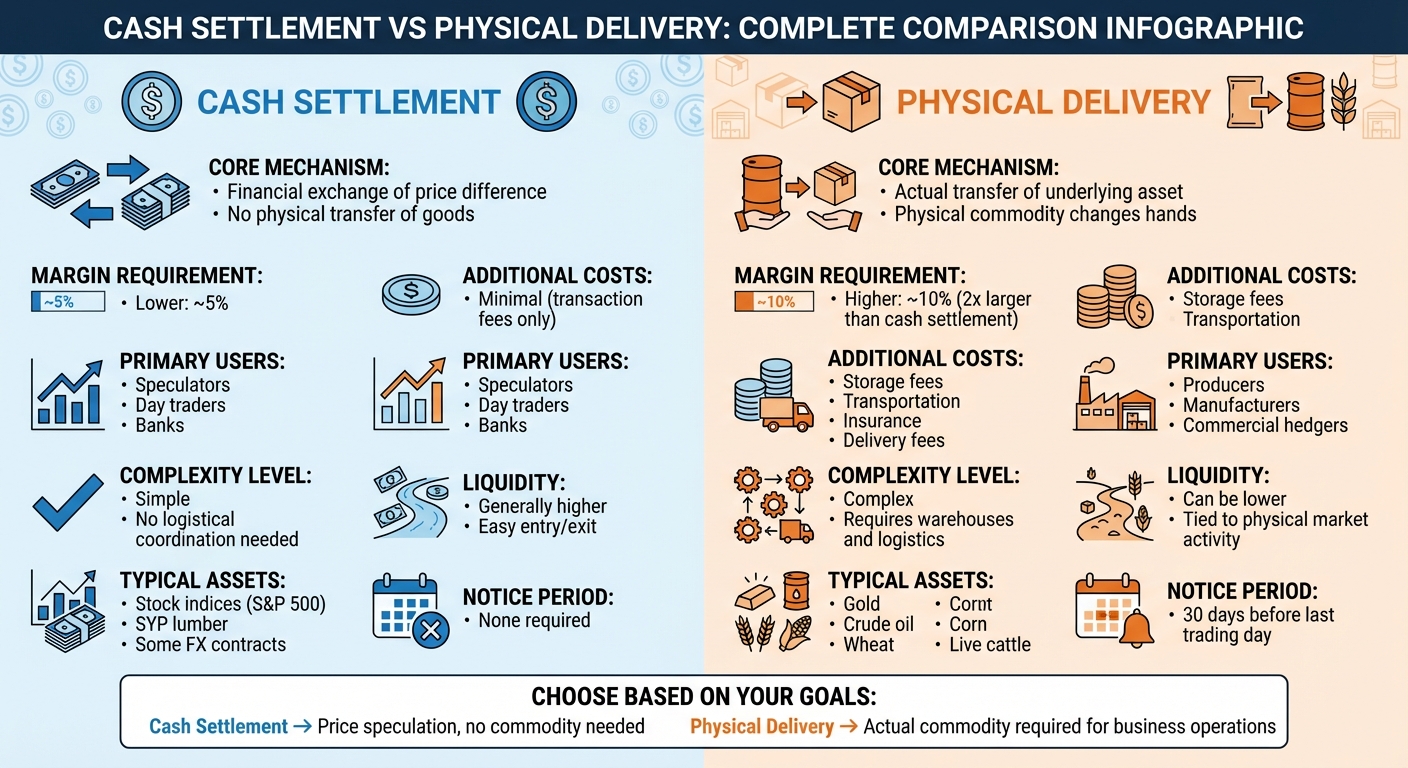

Key Differences Between Cash Settlement and Physical Delivery

The main distinction between cash settlement and physical delivery lies in what gets exchanged when the contract expires. With physical delivery, the actual commodity is transferred to an exchange-approved location, where the buyer takes possession and pays the full contract value. Cash settlement, on the other hand, skips the logistical challenges by calculating a final settlement price – traders only pay or receive the net difference between their entry price and this settlement price.

Margin requirements also differ due to the complexity involved. Cash-settled contracts typically require an initial margin of about 5%, while physically delivered contracts demand closer to 10% of the notional value. Liquidity patterns vary as well. Cash settlement tends to attract more speculators, many of whom trade through the best futures prop firms since there’s no risk of receiving the physical commodity. As CME Group explains:

"Cash settlement allows a greater number of entities to participate late into a contract’s life because the end result is purely a financial exchange rather than optionality on a physical commodity".

In contrast, liquidity for physically delivered contracts often declines as expiration nears because most traders exit to avoid the obligations tied to delivery.

Another key difference lies in cost structures. Cash settlement involves only the net cash difference, with minimal transaction fees. Physical delivery, however, comes with added expenses like storage fees, transportation costs, insurance premiums, and brokerage charges. For traders planning to hold positions requiring physical delivery, maintaining a free-margin buffer of at least 30% is recommended to handle these additional costs. Understanding these financial and logistical differences is critical for choosing the right settlement method for your trading goals and risk management approach.

Comparison Table: Cash Settlement vs Physical Delivery

Here’s a quick breakdown of the differences between the two:

| Feature | Cash Settlement | Physical Delivery |

|---|---|---|

| Core Mechanism | Financial exchange of price difference | Actual transfer of underlying asset |

| Margin Requirement | Lower (typically ~5%) | Higher (typically ~10%) |

| Additional Costs | Minimal (transaction fees only) | Storage, transport, insurance, delivery fees |

| Primary Users | Speculators, day traders, banks | Producers, manufacturers, commercial hedgers |

| Complexity | Simple; no logistical coordination | Complex; requires warehouses and logistics |

| Liquidity | Generally higher due to ease of entry | Can be lower; tied to physical market activity |

| Typical Assets | Stock indices, SYP lumber, some FX | Gold, crude oil, wheat, corn, live cattle |

| Notice Period | None required | Typically 30 days before last trading day |

Use Cases in Futures Trading

When to Use Cash Settlement

Cash settlement works best when physically delivering the underlying asset isn’t practical. For example, stock index futures like the S&P 500 avoid physical delivery because coordinating such logistics would be unrealistic.

This method is especially appealing to speculators and day traders. It allows them to hold positions until expiration without worrying about the complexities of delivery. As CME Group puts it:

"Cash settlement allows a greater number of entities to participate late into a contract’s life because the end result is purely a financial exchange rather than optionality on a physical commodity".

Another key advantage is capital efficiency. For cash-settled contracts, initial margins are typically around 5% (a key factor when comparing profit splits and costs across firms), compared to about 10% for contracts requiring physical delivery. This lower margin requirement means traders can control more contracts with the same amount of capital. However, if you’re trading to acquire the actual commodity for operational needs, physical delivery is the better choice.

When to Use Physical Delivery

Physical delivery is the go-to option for commercial hedgers who need the actual commodity for their business. For instance, grain producers use wheat futures to lock in prices for their harvest, while manufacturers rely on crude oil or gold futures to secure the raw materials needed for production. These participants focus on managing real inventory rather than speculating on price movements.

That said, physical delivery requires careful preparation. Many traders follow strict risk management practices – such as limiting positions to five contracts once the delivery month begins – to avoid being forced into taking delivery unexpectedly.

How Settlement Methods Affect Futures Prop Traders

Finding Prop Firms Based on Settlement Preferences

For most futures prop traders, cash-settled contracts are the go-to choice. Why? Because these traders are interested in price movements, not acquiring physical commodities. This preference plays a big role in deciding which prop firms and account types best align with their strategies.

Cash settlement offers some practical benefits. For instance, the margin requirements are generally around 5% of a contract’s notional value, compared to about 10% for physically delivered contracts. This lower margin allows traders to control more contracts with the same amount of capital, boosting their efficiency.

When choosing a prop firm, tools like DamnPropFirms can help you compare firms based on market and settlement preferences. Some examples include Apex Trader Funding and Take Profit Trader, which provide access to major cash-settled index futures like the E‑mini S&P 500. On the other hand, firms like Topstep and Tradeify offer a broader range of options, including agricultural futures, which may involve physical delivery.

Risk Management Considerations

Managing risk effectively starts with understanding how settlement methods work and choosing prop firms that fit your trading approach. Settlement mechanics are especially important to grasp because they can help you avoid costly errors. For physically delivered contracts, the biggest risk comes from holding a position into the delivery period. Once the initial delivery notice period ends, you could be matched for delivery and obligated to accept – or deliver – the actual commodity.

To steer clear of this risk, always check the settlement method in your platform’s contract details before trading. For physically settled contracts, make sure to roll over your positions in time to avoid delivery obligations. Other tips include limiting exposure to five contracts during delivery periods and maintaining a 30% free-margin buffer to handle unexpected price swings and fees.

For cash-settled contracts, you can reduce risk by setting stop-losses at 1.5 times the Average True Range (ATR) when settlement is near. Additionally, using conditional orders can automate position rollovers, helping you sidestep delivery obligations altogether.

Conclusion: Choosing the Right Settlement Method

When deciding on a settlement method, it’s important to align it with your trading goals and operational capabilities. For speculators and day traders, cash-settled contracts are often the preferred choice. They offer simplicity, lower margin requirements, and avoid the logistical challenges tied to handling actual commodities. This method works best if your focus is on trading price movements rather than dealing with physical assets.

On the other hand, commercial hedgers and producers often rely on physical delivery. This option allows them to lock in prices for actual inventory and ensures they meet their operational needs. However, physical delivery requires infrastructure for storage, transportation, and quality checks. As Alphaex Capital explains:

"Select the settlement method that matches your strategy – hedgers should opt for physical delivery, while day traders benefit from cash-settled contracts".

Understanding how each method works is crucial to avoid costly errors. With cash settlement, the process is straightforward: the price difference is credited or debited from your account. Physical delivery, while practical for certain traders, comes with added costs for storage, insurance, and quality compliance.

Your risk tolerance also plays a key role in this decision. Physical delivery involves higher operational costs, while cash settlement requires confidence in the final settlement price, which is often determined by a Price Reporting Agency or VWAP.

Finally, choosing the right futures prop firm can make a big difference. Platforms like DamnPropFirms offer tools to compare firms such as FundedNext vs FundingTicks and Alpha Futures to find one that aligns with your settlement strategy. Matching your settlement method to your trading approach ensures a smoother and more effective trading experience.

FAQs

How can I tell if a futures contract is cash-settled or physically delivered?

When dealing with contracts, it’s essential to review the specifications provided by the exchange or trading platform. Physically delivered contracts require the actual transfer of the commodity upon expiration. On the other hand, cash-settled contracts are finalized by paying or receiving the net cash difference based on the commodity’s price.

The settlement method is clearly outlined in the contract details. If you’re unsure, refer to the exchange’s rules for additional clarity.

What happens if I accidentally hold a physically delivered contract into the delivery period?

If you keep a physically delivered contract into its delivery period, the physical delivery process kicks off. At this stage, you’ll be paired with a counterparty, and the commodity will be exchanged between the party delivering it and the one receiving it. Any position still open after the close on the first position day qualifies for delivery, and all positions remaining after expiration are required to go through the delivery process.

How is the final settlement price calculated for cash-settled futures?

The final settlement price for cash-settled futures is typically determined by averaging prices over a set period. This might include opening and closing prices from a trading day or prices within a specific time window. For certain agricultural contracts, the price may hinge on screen trading activity. The exact calculation method varies depending on the exchange and the details outlined in the contract.