One MES tick is $1.25. One full point is $5.00. That’s the only math most traders need before they click buy or sell. If you’re sizing futures trades on a small account or inside a prop drawdown, MES keeps the S&P 500 exposure small enough to not blow yourself up on one bad entry.

I’ll keep this clean: what one MES contract controls, how the tick math works, what a 10-point move pays, and how to turn your stop into a dollar risk number. If you trade ES too big, MES is the fix. Same market. Less pain when you’re wrong.

How to Calculate Profit or Loss on Futures Contracts

sbb-itb-46ae61d

What Is the MES Contract?

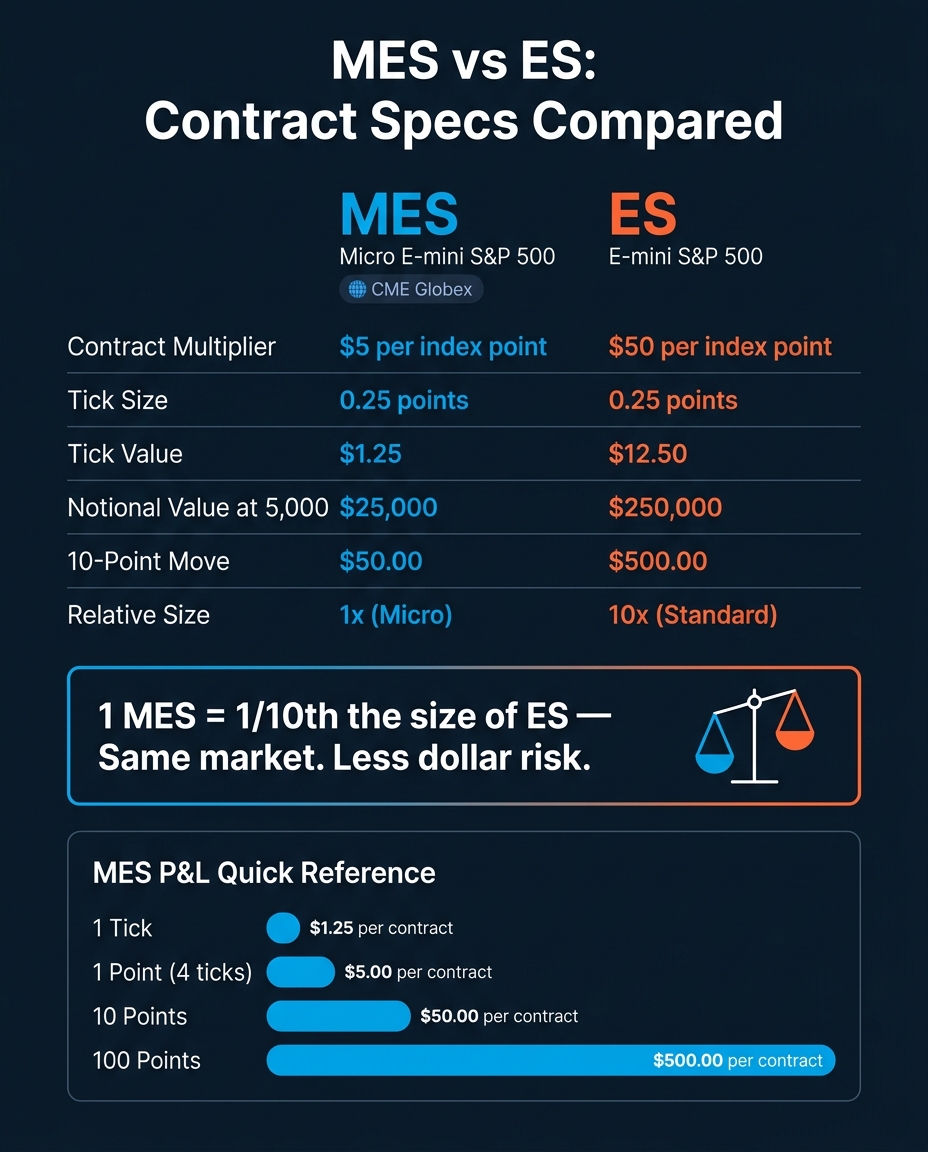

MES vs ES Contract Specs: Key Differences at a Glance

The Micro E-mini S&P 500 (MES) is the smaller S&P 500 futures contract. It uses a $5 multiplier for each index point and settles in cash at expiration. That makes it a much better fit for smaller accounts and tighter risk control.

It’s also easy to line up next to ES because the math is clean. Same market. Same basic price movement. Just a lot less dollar exposure.

MES vs. ES: Key Differences

MES is 1/10 the size of the standard E-mini S&P 500 (ES). Both contracts use the same 0.25-point tick size, but the cash impact is nowhere near the same.

One tick in MES is worth $1.25. That same tick in ES is worth $12.50. So if the market moves 10 points, that’s $50 on MES and $500 on ES.

| Feature | MES | ES |

|---|---|---|

| Contract Multiplier | $5 per index point | $50 per index point |

| Tick Size | 0.25 points | 0.25 points |

| Tick Value | $1.25 | $12.50 |

| Example Notional Value at 5,000 | $25,000 | $250,000 |

That size gap is the whole point. MES gives you the same S&P 500 exposure structure as ES, just in a smaller chunk. This is similar to how the MNQ contract specs provide a smaller alternative to the standard Nasdaq futures.

Contract Multiplier and Notional Value

MES notional value is simple:

S&P 500 index level × $5

So if the index is at 5,000, one MES contract gives you $25,000 in notional exposure.

From there, the next step is to break it down into tick size, tick value, and point value.

How Much Is One MES Tick Worth?

Price movement is your P/L. Simple as that. For MES, you can do the math in ticks or points. Same answer either way.

MES Tick Size

The minimum price move for MES is 0.25 index points.

MES Tick Value and Point Value

Each 0.25-point tick is worth $1.25 per contract. One full 1.00-point move is worth $5.00 per contract.

| MES Move | Ticks | Index Points | Dollar Value (1 Contract) |

|---|---|---|---|

| 1 Tick | 1 | 0.25 | $1.25 |

| 1 Point | 4 | 1.00 | $5.00 |

| 10 Points | 40 | 10.00 | $50.00 |

| 100 Points | 400 | 100.00 | $500.00 |

So if MES moves 10 points, that’s $50 per contract. The same move in ES is $500. Same index move. 10x less dollar risk on MES.

MES P/L Formulas

Use either formula below. They give you the same result.

P/L = ticks × $1.25 × contracts

P/L = points × $5.00 × contracts

Example: if you’re long 2 MES contracts and price moves up 4.50 points, your profit is $45.00.

That math also matters before you enter a trade. It’s how you size risk and figure out what your stop will cost.

How to Calculate MES Profit and Loss

Use the formulas above to turn MES price moves into actual dollar P/L.

1-Tick, 4-Tick, and 10-Point Move Examples

This is where the math gets practical. A 1-tick move in MES is 0.25 index points, which means $1.25 gained or lost per contract. A 4-tick move equals 1 full point, or $5.00 per contract. If MES moves 10 points, that’s $50.00 per contract.

Nothing fancy here. MES pays in small increments, and those small increments stack up fast when you add contracts.

How P/L Changes With Multiple Contracts

P/L scales in a straight line with contract count. Double the contracts, double the P/L. Same move. Same math.

| Move | 1 Contract | 2 Contracts | 3 Contracts | 5 Contracts |

|---|---|---|---|---|

| 1 Tick (0.25 pts) | $1.25 | $2.50 | $3.75 | $6.25 |

| 4 Ticks (1 Point) | $5.00 | $10.00 | $15.00 | $25.00 |

| 20 Ticks (5 Points) | $25.00 | $50.00 | $75.00 | $125.00 |

| 40 Ticks (10 Points) | $50.00 | $100.00 | $150.00 | $250.00 |

Commissions still take a bite. Round-trip MES commissions run about $1.82 per contract [1]. So if you catch a 4-tick scalp with 3 contracts, your $15.00 gross gets cut by $5.46 in commissions, leaving $9.54 net.

That’s the part a lot of traders gloss over. On small MES moves, fees matter a lot.

How to Size an MES Position for Risk

Knowing the tick value is only half the job. The other half is figuring out how many MES contracts you can trade before the risk gets stupid.

Calculate Dollar Risk From Your Stop Loss

The formula is simple: Position Size = Max Dollar Risk ÷ (Stop Loss Distance in Ticks × $1.25).

Here’s the math. If your stop is 8 ticks (2 points) from entry and you want to risk $20, the setup looks like this:

$20 ÷ (8 × $1.25) = $20 ÷ $10 = 2 contracts

If the stop is tighter, like 4 ticks, you can trade 4 contracts and still keep the same $20 risk. That’s the whole point. As the stop gets wider or tighter, your size changes, but your risk stays fixed.

On prop firm accounts, don’t size off the headline balance. Size off the drawdown limit. That’s the number that matters. On a $50,000 prop firm account with a $2,000 drawdown limit, risking 1% per trade means risking only $20 [1]. That’s why this formula matters. It stops one bad trade from taking too big a bite out of your drawdown.

Use the result to pick your contract count.

| Max Risk | Stop Distance | Max MES Contracts |

|---|---|---|

| $20 | 4 ticks (1 point) | 4 contracts |

| $20 | 8 ticks (2 points) | 2 contracts |

| $20 | 16 ticks (4 points) | 1 contract |

| $50 | 10 ticks (2.5 points) | 4 contracts |

That’s where MES shines. It keeps your dollar risk small enough to control without forcing you into goofy stop placement.

Using MES to Reduce Exposure

Once you’ve set size from the stop, MES gives you tighter control over execution. Smaller contract size means more room to trade the setup the way it should be traded.

You can place a stop based on market structure, not just on what your account can survive. That’s a big deal. A stop under a swing low or over a swing high makes more sense than jamming it into some random spot just to shrink dollar risk.

MES also lets you keep similar market exposure with less dollar risk, and you can scale out 1 contract at a time. That’s cleaner trade management. No need to dump the whole position at once if you want to take partials.

MES Trading Hours and Contract Months

Once you know your MES dollar risk per contract, the next thing that matters is when you trade it. Timing changes everything. A setup that looks clean during RTH can feel sloppy and thin overnight.

MES Trading Hours on CME Globex

MES futures trade on CME Globex almost 24 hours a day, five days a week. The week starts Sunday at 6:00 PM ET and ends Friday at 5:00 PM ET. There’s also a daily maintenance halt from 5:00 PM to 6:00 PM ET, Monday through Thursday, when the market is closed.

MES trades in both ETH and RTH, but RTH is usually where you want to be if you care about cleaner fills. ETH is thinner. RTH tends to have the tightest spreads and the most liquidity.

RTH runs from 9:30 AM to 4:15 PM ET. The busiest windows are usually:

- 9:30–10:30 AM ET, right after the open

- 3:30–4:00 PM ET, into the close

That’s where you’ll often see the biggest moves. It’s also where things can get wild fast. Major data releases can widen spreads and increase slippage, so don’t act surprised if your fill looks worse than expected during those moments.

After session timing, the next contract detail that matters is the month you’re trading.

MES Contract Months

MES uses a quarterly expiration cycle. There are four contract months each year:

| Contract Month | Code | Expiration |

|---|---|---|

| March | H | Third Friday of March |

| June | M | Third Friday of June |

| September | U | Third Friday of September |

| December | Z | Third Friday of December |

Each one expires on the third Friday of that month. In most cases, you should trade the front month because that’s where the liquidity is.

Those month codes aren’t just trivia. The active contract shifts as expiration gets closer, and if you’re looking at the wrong one, volume can dry up fast.

Rollover and Expiration Basics

Rollover means closing your position in the expiring contract and reopening it in the next contract month. For MES, the standard move is to roll on the Monday before the third Friday of the expiration month [1].

If you hang around too close to expiration, spreads can widen and price gaps can show up [1]. That’s just unnecessary friction. MES is cash-settled, so gains and losses are settled in cash at expiration [3][4]. Rolling on time keeps you in the contract with the best liquidity.

MES Contract Specs Reference Table

Once you know your stop distance and target, this table gives you the MES math at a glance.

| Specification | Detail |

|---|---|

| Ticker Symbol | MES |

| Exchange | CME (Chicago Mercantile Exchange) |

| Contract Multiplier | $5 × S&P 500 Index |

| Tick Size | 0.25 index points |

| Tick Value | $1.25 per tick |

| Point Value | $5.00 per point |

| Trading Hours | Sun 6:00 PM – Fri 5:00 PM ET (Daily break: 5:00 PM – 6:00 PM ET) |

| Contract Months | March (H), June (M), September (U), December (Z) |

| Settlement Type | Cash-settled |

Use these specs to turn chart movement into dollar risk and reward.

Common MES price moves per contract:

| Move | Ticks | Dollar Value (1 Contract) |

|---|---|---|

| 1 tick | 1 | $1.25 |

| 1 point | 4 | $5.00 |

| 8-tick stop | 8 | $10.00 |

| 10-point target | 40 | $50.00 |

| 50-point move | 200 | $250.00 |

That’s the part a lot of newer futures traders miss. On MES, small chart moves stay pretty small in dollar terms. A 1-point move is $5.00 per contract. A 10-point target is $50.00. Clean. Easy to map out before you click in.

Bottom Line: What One MES Contract Means for Your Trading

Boil it down to the only numbers that matter: $1.25 per tick and $5.00 per point. So if MES moves 10 points, that’s $50.00 per contract.

That’s the math behind your risk on every single trade. No fluff. If your drawdown limit is fixed, this gap matters. Traders using The Futures Desk prop firm benefit from no intraday drawdowns, making these calculations even more critical for managing risk. A 20-point move against you is a $100 hit on one MES contract[2]. On the flip side, MES gives you smaller sizing steps, which makes it easier to scale in without going too big too fast.

Small scalps need clean math too. If your average win barely clears commissions and fees, you’re grinding for nothing.

Use $1.25 per tick and $5.00 per point every time you size a trade.

FAQs

How much margin do I need to trade one MES contract?

In a personal brokerage account, day-trading margin for one Micro E-mini S&P 500 (MES) contract is usually $40 to $50.

With a futures prop firm, you’re not dealing with margin the same way. The firm handles risk with position limits and drawdown rules instead. If your account balance drops below the firm’s set threshold, that can trigger a breach.

When should I switch to the next MES contract month?

Switch to the next MES contract month on the Monday before the third Friday of the expiration month. MES expires every quarter: March, June, September, and December.

That rollover date matters. By then, volume and liquidity have usually moved out of the expiring contract and into the new front month. If you’re still sitting in the old contract, fills can get worse and the market can feel thin.

In plain English: close the position in the expiring contract, then open the same trade in the next contract month.

Is MES better than ES for small accounts?

Yes. MES is usually the better pick for small accounts and newer traders because it’s 1/10 the size of ES. That gives you tighter control over position size and risk.

Here’s the part that matters: ES pays $12.50 per tick, while MES pays $1.25 per tick. That smaller exposure makes it a lot easier to keep losses in check and avoid the kind of oversized trade that smacks your account with a nasty drawdown.