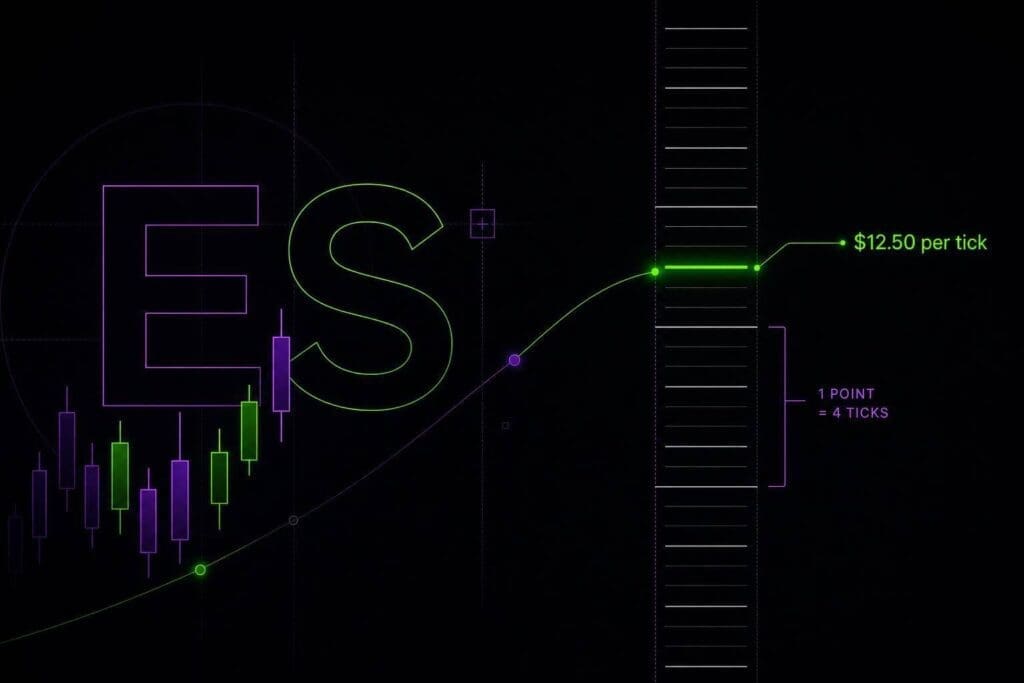

One ES tick is $12.50. That’s the number that runs the whole trade. Since ES moves in 0.25-point steps and each full point is $50, you can price your stop, target, and contract count fast before you hit the button. If you trade index futures, this is the part you need locked in.

I’m going to keep this tight: the core ES specs, what one contract controls at common index prices, how to turn ticks into dollar risk, and when ES is just too damn big so you should use MES instead. No fluff. Just the math that keeps you from sizing like an idiot.

How to Calculate Profit or Loss on Futures Contracts

Introduction

The E-mini S&P 500 futures contract (ES) trades on CME Globex at $50 per index point and $12.50 per tick. Those two numbers control every ES risk call you make.

The math is simple: notional value = index level × $50. So if ES is at 5,000, one contract is about $250,000 in notional exposure.

Know what each tick is worth in dollars before you enter. Next up: exchange, symbol, contract size, tick size, and trading hours.

Table of Contents

- ES Contract Specs on CME

- How Much Is One ES Tick Worth in Dollars?

- How to Size Risk on ES Using Tick Value

- ES Trading Hours and How Session Timing Affects Risk

- ES vs. MES: When to Size Down With Micros

- ES Rollover and Expiration: What Traders Need to Know

- ES Tick Value: The Numbers to Remember

ES Contract Specs on CME

ES trades on CME Globex through CME. Simple math matters here: every move in ES turns into a fixed dollar gain or loss per contract [1][2]

Exchange, Symbol, and Contract Size

ES is the ticker for the E-mini S&P 500 futures contract. The full contract name uses the ES symbol, a month code, and a two-digit year [1][7]

The contract uses a $50 multiplier per index point. It’s also cash settled to the S&P 500’s final settlement value, so there’s no stock delivery nonsense at expiration [1][4]

Tick Size, Tick Value, and Point Value

| Specification | Detail |

|---|---|

| Exchange | Chicago Mercantile Exchange (CME) |

| Ticker Symbol | ES |

| Contract Size | $50 × S&P 500 Index |

| Minimum Tick | 0.25 index points |

| Tick Value | $12.50 per contract |

| Point Value | $50.00 per contract |

| Settlement | Cash settled |

Source: cmegroup.com

That pricing ladder is the part you need burned into your brain:

- 1 tick = 0.25 points = $12.50 per contract

- 1 point = 4 ticks = $50.00 per contract

So if ES moves 2 points, that’s $100 per contract. If it moves 10 ticks, that’s $125 per contract. Clean and predictable.

Contract Months and Trading Hours

ES expires on the quarterly cycle: March, June, September, and December [1][4]

| Session | Time (CT) |

|---|---|

| Sunday Open | 5:00 PM |

| Monday–Thursday Close / Reopen | 4:00 PM / 5:00 PM |

| Friday Close | 4:00 PM |

| Regular U.S. Cash Session | 8:30 AM – 3:15 PM |

Source: cmegroup.com

ES trades nearly around the clock, with the usual one-hour daily pause from 4:00 PM to 5:00 PM CT Monday through Thursday. The main U.S. cash session runs from 8:30 AM to 3:15 PM CT, which is when a lot of traders focus on volume and cleaner moves.

Next, convert these specs into dollar P&L per tick and per contract.

How Much Is One ES Tick Worth in Dollars?

One ES tick is worth $12.50 per contract. Four ticks make 1 full point, which equals $50 per contract. If you trade ES, that’s the math you need burned into your brain.

Use the examples below to turn ES price moves into dollar P&L fast.

ES Tick-to-Dollar Examples

| Movement | Ticks | Points | Value (1 Contract) |

|---|---|---|---|

| Minimum tick | 1 | 0.25 | $12.50 |

| Half point | 2 | 0.50 | $25.00 |

| Full point | 4 | 1.00 | $50.00 |

| 2-point move | 8 | 2.00 | $100.00 |

| Large move | 40 | 10.00 | $500.00 |

That same math carries straight over to multi-contract trades. No trick to it. Just multiply by the number of contracts.

P&L for Multiple Contracts

For 2 contracts, a 10-point move equals $1,000. For 5 contracts, the same move equals $2,500.

Formula: ticks × $12.50 × contracts

If you think in points instead of ticks, that works too:

- 1 point = $50 per contract

- 10 points = $500 per contract

- Then multiply by your contract size

Unrealized vs. Realized P&L on Futures Platforms

Open trades show unrealized P&L. Once you close the trade, it becomes realized P&L.

That matters more than some traders think. Futures are marked to market each day, so gains and losses get posted to your margin account at the end of the trading session [1][7]. On a platform or eval with an intraday drawdown rule, your live unrealized P&L can cut into your remaining drawdown room before you even exit the trade.

In plain English: if your position goes against you, that floating loss still counts for risk. That’s the number intraday limits react to.

sbb-itb-46ae61d

How to Size Risk on ES Using Tick Value

Once you know an ES tick is worth $12.50, you can turn that into actual trade risk. That’s the part that matters. Don’t place the order first and do the math later.

Converting Stop Distance Into Dollar Risk

Dollar risk per contract = stop points × $50, or ticks × $12.50. Run that number before you enter.

| Stop Distance | Ticks | Dollar Risk (1 Contract) |

|---|---|---|

| 2 points | 8 | $100.00 |

| 5 points | 20 | $250.00 |

| 10 points | 40 | $500.00 |

A 5-point stop means $250 at risk on one ES contract. A 10-point stop means $500 at risk per contract. That adds up fast.

Position Sizing Examples for Small Accounts

Max contracts = max trade risk ÷ risk per contract.

Say your max loss on a trade is $300 and your stop is 5 points ($250 per contract). You can trade 1 contract and stay inside your limit. Go to 2 contracts, and now you’ve got $500 at risk. That’s over budget.

| Max Trade Risk | Stop Size | Max Contracts |

|---|---|---|

| $150 | 5 points ($250/contract) | No ES contract fits |

| $300 | 5 points ($250/contract) | 1 |

| $500 | 5 points ($250/contract) | 2 |

| $500 | 2 points ($100/contract) | 5 |

This is why small accounts get in trouble with ES. The contract isn’t forgiving. A stop that looks normal on the chart can still hit your risk cap fast.

Why Tick Value Matters for Drawdown and Daily Loss Limits

Start with stop risk. Then size the position.

At $12.50 per tick, even a small move against you can chew through drawdown or a daily loss limit fast. If you work backward from your max risk, you cut out the dumb mistake of oversizing.

Risk also shifts with session liquidity, which matters next.

ES Trading Hours and How Session Timing Affects Risk

ES trades almost 24 hours a day on CME Globex, but don’t treat every hour the same. The tick value stays fixed at $12.50. What changes is how well you get filled.

Globex Overnight vs. Regular Trading Hours

The big split is overnight Globex versus RTH.

| Session | Hours (ET) | Liquidity | Typical Spread |

|---|---|---|---|

| Globex Overnight | 6:00 PM – 9:30 AM | Lower | Wider |

| Regular Trading (RTH) | 9:30 AM – 4:15 PM | Highest | 1 tick ($12.50) |

| Daily Break | 5:00 PM – 6:00 PM | Closed | N/A |

RTH is where ES gets its deepest liquidity. During RTH, the bid-ask spread is usually just 1 tick ($12.50) [6]. Overnight, spreads get wider, and thinner order books can lead to more slippage.

Why the Same Tick Value Feels Different by Session

The math does not change. One tick is $12.50 whether it’s 2:00 AM or 10:00 AM ET. What changes is execution.

During RTH, especially the 9:30–11:00 AM ET window, liquidity is tighter, spreads are narrower, and stops usually fill closer to your price. Overnight, the book gets thinner. That means a market order can slip several ticks from the last price you saw. Same tick value. Different fill quality.

Keep it simple:

- Trade smaller during thin sessions.

- Use limit orders if you want tighter control over slippage.

- Overnight is thinner. RTH is cleaner.

Once session timing is clear, the next step is figuring out whether ES or MES fits your risk better.

ES vs. MES: When to Size Down With Micros

ES vs. MES Futures: Contract Specs Comparison

If ES is too big for your risk limit, MES gives you the same S&P 500 exposure at one-tenth the dollar value. That’s the whole point. When your stop is tight, ES can get clunky fast, while MES stays workable.

ES and MES Specs Side by Side

The main split is the multiplier: ES is $50 per point. MES is $5 per point.

| Specification | ES (E-mini S&P 500) | MES (Micro E-mini S&P 500) |

|---|---|---|

| Contract Multiplier | $50 × Index | $5 × Index |

| Tick Size | 0.25 points | 0.25 points |

| Tick Value | $12.50 | $1.25 |

| Point Value | $50.00 | $5.00 |

| Notional Value (S&P at 5,000) | $250,000 [3] | $25,000 [3] |

That gap is why MES usually makes more sense for smaller accounts.

When MES Makes More Sense Than ES

Use MES when ES tick risk is too high for your stop or your drawdown limit. Simple as that. If the stop you need on ES blows past your risk cap, drop down to MES.

Here’s the math. A 6-tick stop on ES risks $75. The same 6-tick stop on one MES risks $7.50 [2]. Same market. Same chart. Way less dollar risk.

MES also gives you finer position sizing. That helps when you want to scale in, scale out, or take partials without forcing the trade. ES jumps in bigger chunks. MES lets you be more precise.

ES Rollover and Expiration: What Traders Need to Know

After tick value, the next thing that matters is simple: are you trading the right ES contract? ES is cash settled at expiration, so your P&L is based on final settlement, not delivery [1][4][8]. For most traders, that means keeping your focus on the active front-month.

Quarterly Expiration Cycle and Front-Month Selection

ES runs on a four-contract cycle each year: March (H), June (M), September (U), and December (Z) [1][2][4]. The front-month is the nearest contract to expire, and it usually carries the most volume.

That’s the one intraday traders want. More volume usually means tighter spreads, deeper books, and less slippage getting in and out [1][2]. If you’re scalping or trading size, that matters a lot.

When Traders Roll to the Next Contract

Rollover usually begins in the week before expiration. That’s when volume and open interest start moving from the expiring contract into the next one, and spreads in the old contract often get worse [2][5][6].

The main tell is volume. Once the next contract starts trading more volume than the current one, that’s usually your signal that the new month is now the active market [2][5]. Open interest can help confirm the move [1][4].

Don’t wait until the old contract gets thin. Thin books mean more slippage. Bad fills add up fast.

Use the CME expiration calendar to check the exact roll timing, because holiday schedules can shift the window [5].

The rollover changes liquidity, not tick value.

ES Tick Value: The Numbers to Remember

For ES sizing, keep two numbers in your head: $12.50 per tick and $50.00 per point [2].

Before you enter, do the math:

Dollar risk = ABS(Entry Price − Stop Price) × $50 × contracts

That tells you what the trade will cost if your stop gets hit. Simple. No guesswork.

If that number is over your risk limit, don’t force ES. Drop to MES instead.

At the end of the day, ES risk math is just this: $12.50 per tick and $50.00 per point. Burn those into your brain.

FAQs

How much margin do I need to trade one ES contract?

In a personal futures account, margin for 1 ES contract depends on one thing first: are you flat by the close, or are you holding overnight?

If you’re day trading, the broker sets the intraday margin. That’s often around $400 to $500 per contract. Cheap on paper. But that only works if you close the trade before the broker’s cutoff.

If you hold the position overnight, you’re in a different lane. Then you need to meet the exchange initial margin, which can be about $13,000, with maintenance margin around $12,000. And yeah, those numbers move when volatility picks up. A calm market and a wild market don’t get treated the same.

Prop firm accounts work differently. You usually don’t deal with margin in the old-school retail sense. Instead, the firm controls risk through position limits and drawdown rules. So rather than asking, "What’s the ES margin?" the better question is, "How many contracts can I hold, and how much room do I have before I hit the drawdown?"

What’s the difference between notional value and actual cash risk in ES?

Notional value is the full face value of the position you control: current index level × the $50-per-point multiplier. If ES is at 6,000, one contract carries a notional value of $300,000.

Actual cash risk is what you stand to lose if price moves against you and hits your stop. Since ES ticks are worth $12.50 each, an 8-tick stop puts $100 at risk per contract.

How do I know when to switch from MES to ES?

Consider switching once you’ve been consistently profitable on MES for at least 4 straight weeks.

Before you move to ES, you should know your average win and loss in ticks, and you should be able to figure out your per-trade risk in your head. No calculator. You also need to be fine with the bigger dollar swings: $12.50 per tick on ES vs. $1.25 on MES.

This is a sizing shift. Not a strategy shift.